Monthly Recap

In the first half of the year, the stock market experienced a stellar run, primarily driven by mega-cap technology stocks. However, since the end of July, there has been a pullback. This shift occurred as progress on disinflation slowed, while economic data remained robust, and the U.S. government’s massive debt issuance roiled the bond market. October, the first month of the fourth quarter, saw similar trends in both stock and bond markets. The S&P 500 Index decreased by 2.1%, and the smaller cap Russell 2000 Index fell by 6.8%. The top 50 stocks declined by only 1.3%, while the average stock in the S&P 500 Index dropped by 4.1%.

Over the course of the month, value stocks—represented by the Russell 3000 Value Index—declined by 3.7%. In contrast, their growth counterparts saw a milder decline of just 1.7%. This disparity can be attributed to the dominance of mega-cap growth stocks within growth indices. These stocks typically have a substantial cash reserve and minimal debt, making them more resilient to rising interest expenses compared to value stocks.

On the sector front, all sectors experienced a decline with two exceptions: Utilities and Technology, which posted gains of 1.3% and 0.1%, respectively. The most affected sectors were Energy and Consumer Discretionary, which dropped by 5.8% and 5.5%, respectively during the month.

In the bond market, the 10-year U.S. Treasury yield persisted in its upward trajectory, surging from 4.57% at the beginning of the month to nearly 5.00% by October 19, 2023 only to conclude the month at 4.93%. It is important to note that as yields rise, bond prices typically fall. Throughout October, all Treasury maturities witnessed a decline in value, with longer-term bonds experiencing the most significant sell-offs. Higher duration strategies also proved ineffective within the corporate bond sector. However, short-term corporate bonds outperformed, as the benefits from high coupon rates outweighed the price declines.

Market Drivers

The primary drivers influencing both stock and bond markets included rising rates, stretched valuations, a hawkish stance from the Federal Reserve (Fed), and a ballooning Federal deficit that led to a substantial issuance of bonds by the U.S. Treasury. These rising rates can be attributed to a confluence of factors: the increasing supply of bonds due to the aforementioned deficit, robust economic data fueled by consumer spending, the Federal Reserve’s guidance hinting at higher for longer interest rates, and the hawkish pivot by the Bank of Japan. The latter’s decision to exit their decade-long ultra-accommodative policy resulted in diminished foreign demand for U.S. Treasuries.

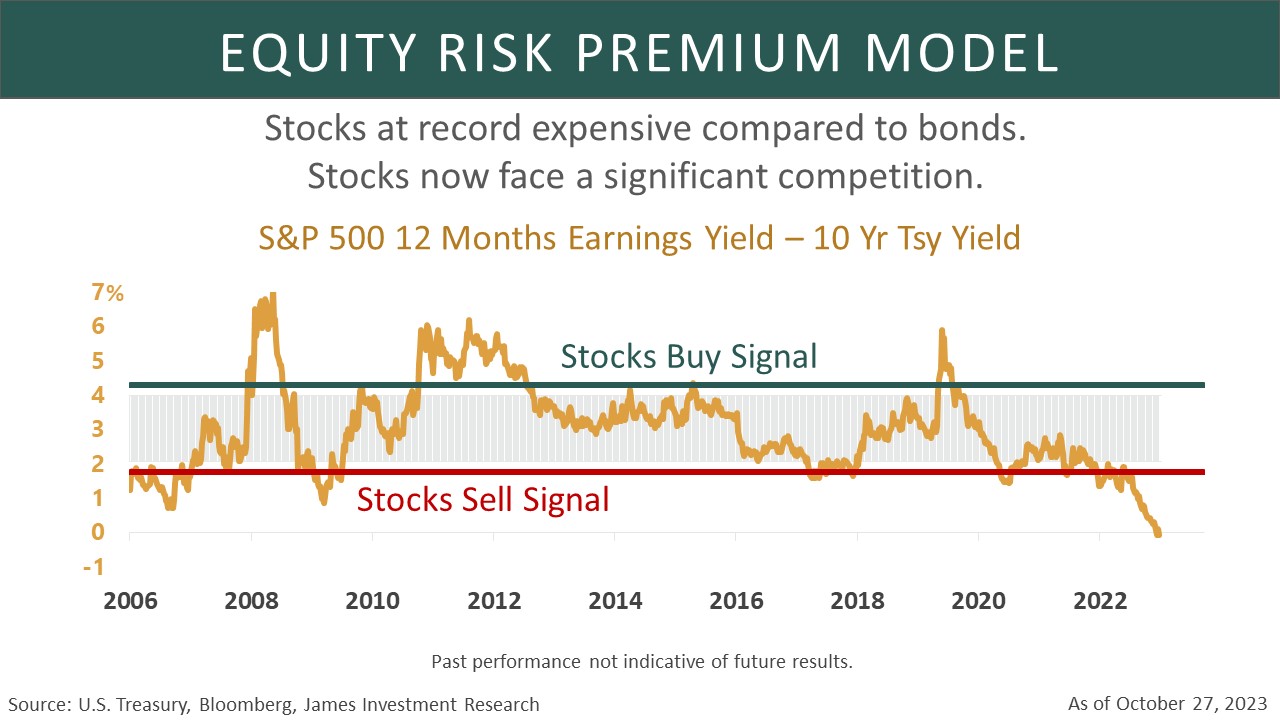

Within the stock market, valuations appear stretched, particularly when contrasted with the prevailing interest rates. The equity risk premium, which represents the additional yield an investor receives by opting for risky stocks over the guaranteed yield of risk-free Treasuries, is at its lowest level in over two decades. As a result, stocks now face significant competition.

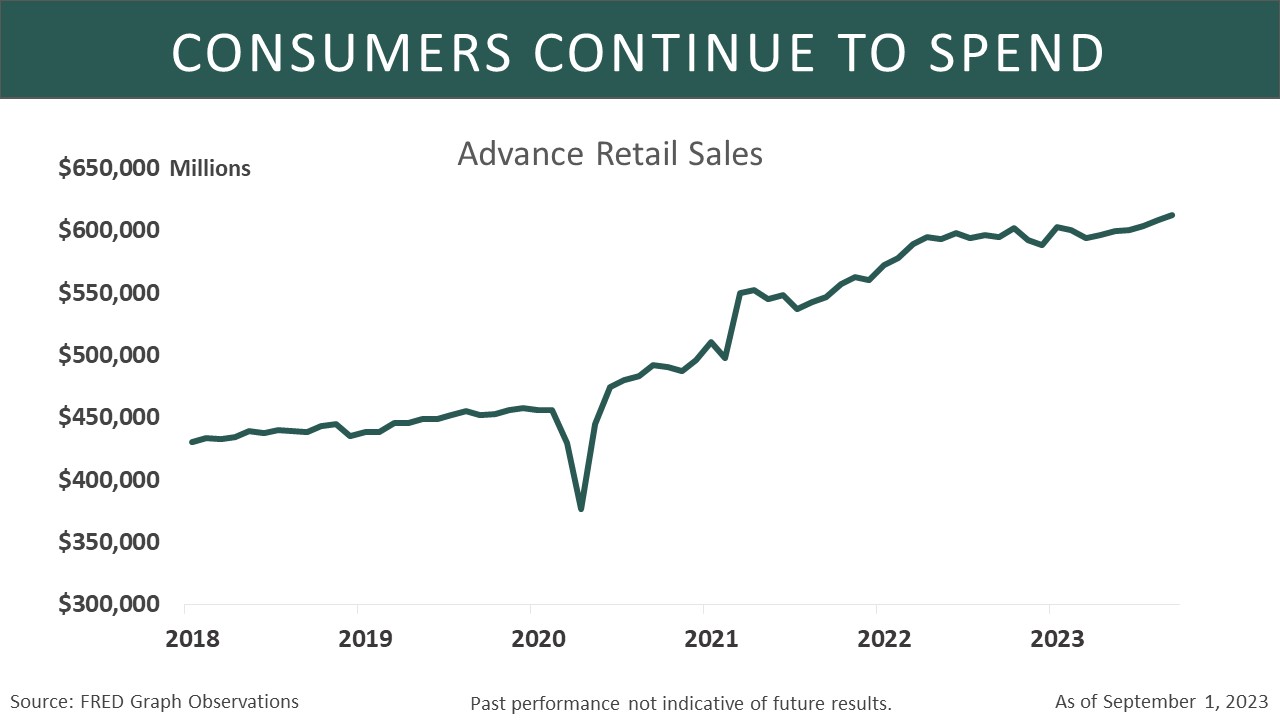

In addition, a resilient labor market combined with excess savings has fueled consumer spending over the summer, causing economic data to frequently exceed most economists’ expectations. Even with the challenges posed by rising interest rates, stubborn inflation, and a moderating labor market, the American consumer has demonstrated remarkable resiliency, pushing household spending to impressive levels.

September’s retail sales report was a testament to this trend, showcasing 0.7% month-over-month growth. Notably, there was a marked increase in sales for online retailers, car dealerships, health, and personal care stores, and dining establishments, underscoring the prevailing shift towards experiential consumption.

A more robust economy, however, does carry the risk of further fueling inflation and prompting a more hawkish stance from the Federal Reserve, which could translate into escalating interest rates. Despite significant strides in tapering inflation from the stark 9.1% Consumer Price Index (CPI) reading in June 2022, the momentum of this disinflation has decelerated in recent times. This is particularly evident in headline inflation, swayed by the oil price upticks throughout the summer.

Looking Ahead to Year-End

Several catalysts have the potential to stabilize both the bond and stock markets: 1) interest rate adjustments, 2) changes in the supply of U.S. Treasury bonds, 3) positive revisions in earnings, and 4) favorable seasonality.

Interest Rates

In recent months, investors have witnessed a rapid increase in yields due to persistent high inflation, robust economic growth, and government deficits affecting Treasury supply. They are now coming to terms with the possibility that interest rates might stay elevated for a prolonged duration.

Over the past month, the Federal Reserve’s signal to maintain current rate levels through 2024 has weighed on both stock and bond prices. The yield on the 10-year U.S. Treasury note soared to its highest point since 2007, exceeding 5.0%. Coupled with potential growth in term premiums, this development might signal a pivotal moment in the Fed’s rate hike trajectory. Some argue that this uptick in yields is assisting the Fed in tightening financial conditions. Rising borrowing costs for businesses and the highest mortgage rates since 2000 are just two examples of the economic repercussions of these escalating yields.

Surprisingly, even with the spike in yields, the economy has demonstrated resilience. Economic indicators consistently exceed expectations, and forecasts of a recession remain unrealized. Consequently, bond traders are reevaluating their predictions for the Fed’s monetary policy.

U.S. Treasury Bond Supply

The August U.S. Treasury Quarterly Refunding Announcement (QRA)—where the U.S. Treasury disclosed the volume of debt it plans to issue over the subsequent three months , acted as the catalyst for the recent bond market tantrum. In that disclosure, the Treasury opted to raise funds by issuing a greater volume of longer-term bonds in contrast to shorter-term Treasury bills and notes. A staggering $671 billion in coupon bonds was issued. This substantial supply contributed to bond investors demanding a higher term premium (the added yield required to hold a longer-term bond compared to a 1-year Treasury Bill). Since that announcement, yields on both 10-year and 30-year Treasuries have surged by nearly 100 basis points, leading to further bond losses.

However, in Quarterly Refunding Announcement (QRA) on November 1st, the U.S. Treasury chose to issue more 2 to 7-year notes than 10 to 30-year bonds, a decision likely to reduce bond volatility. This move has the potential to stabilize the bond market and could potentially trigger a bond rally, especially if economic data begins to show signs of cooling down. This, in turn, might bolster a rally in stocks, as lower interest rates often serve as a tailwind for valuation expansion.

Additionally, we believe current market conditions are conducive to a year-end rally due to several factors:

- a) Technical indicators suggest that both bond and stock markets are oversold.

- b) Investor sentiment is bearish, presenting a contrarian buying opportunity.

- c) Earnings growth is trending positive.

- d) The Federal Reserve might stay its course, as elevated long-term yields could be accomplishing its objectives.

- e) Historically, November and December have been favorable months for the markets.

Earnings Revision

As of this writing, earnings season is in full swing. With just 49% of S&P 500 Index companies having reported, earnings are slightly surpassing expectations. The frequency and scale of positive earnings surprises are above their 10-year averages. According to FactSet, eight out of the eleven sectors are either reporting or projected to report year-over-year earnings growth. Leading the pack are the Communication Services, Consumer Discretionary, and Financials sectors.

Crucially, earnings revisions—indicating how current 12-month earnings estimates stack up against those from three months prior—are positive and on an upward trend. This serves as a reliable barometer of shifting expectations. Historically, a positive uptick in earnings revision has often paved the way for robust future market returns.

Seasonality is Becoming a Tailwind

Market seasonality refers to the propensity of financial markets to follow predictable patterns or trends during specific periods of the year. Historically, markets have often faced challenges advancing during August, September, and the first half of October—a pattern that held true this year. However, November and December have historically seen gains over 70% of the time since 1950. This probability increases if the market performed positively in the year leading up to November.

While the seasonality perspective is compelling, it is essential to consider it in tandem with current macroeconomic and market conditions, as these are the primary market drivers.

Near-Term Risks to the Market

There are notable risks to this optimistic perspective. These encompass hostile geopolitical dynamics, especially if the Middle East conflict escalates regionally, profoundly affecting oil prices. In addition, the U.S. Treasury might persist in skewing its significant debt issuance towards longer-term bonds. This could further drive-up yields, thereby curbing any potential upswing in the stock market.

Furthermore, should the economy maintain its momentum throughout the 4th quarter, the Fed might feel compelled to hike interest rates even further to temper the pace and align inflation with its targets. While this is not our base case—we anticipate that elevated interest rates will significantly decelerate the economy in the 4th quarter—we don’t forecast a recession during that period.

Topic of the Month: Geopolitical Risks

After a period of relative tranquility in the Middle East and growing indications that Saudi Arabia might recognize Israel, tensions escalated abruptly following Hamas’ attack on October 7th. Israel’s decisive response heightened the situation. This unexpected conflict forced investors to face new global political challenges stemming from the hostilities between Hamas and Israel.

Analysts are currently assessing two primary trajectories for the conflict between Israel and Hamas. The first scenario envisions a contained conflict that remains largely between the two immediate parties, without significant intervention from other nations. As of now, financial markets seem to have priced in this more localized confrontation. Historical precedents, such as the short-lived Gaza wars of the past, suggest that the repercussions on the financial markets from such localized conflicts are temporary and often moderate.

The second, more concerning scenario postulates a wider war that could potentially draw in regional powers like Iran. If this were to occur, the implications for the global economy could be profound. Specifically, oil prices might witness a substantial surge. Iranian oil production, which constitutes about 2% of global output, would likely be disrupted. Moreover, the Strait of Hormuz, a critical waterway responsible for the transit of roughly 20% of global oil supplies, could face blockades in the event of hostilities involving Iran. This blockade would have far-reaching consequences, not only for oil prices but for the broader global economy as well.

As geopolitical tensions mount, the global financial structure is potentially at risk, threatened by looming inflation and a slowing pace of growth, according to a warning from the Federal Reserve last Friday. In its latest biannual Financial Stability Report, the U.S. central bank highlighted the potential for “broad adverse spillovers to global markets,” particularly if conflicts in regions such as the Middle East and Ukraine intensify.

The report mentioned, “Escalation of these conflicts or a worsening in other geopolitical tensions could disrupt global economic activity and amplify inflation, especially if supply chains experience prolonged disruptions and there are interruptions in production.”

Furthermore, the Bank emphasized that “The global financial system may face challenges arising from a decrease in risk-taking, asset price declines, and potential losses for businesses and investors, including those in the U.S.”

Historical events in the Middle East, especially the 1973 Yom Kippur War followed by the Arab oil embargo, have indelibly marked the memories of investors. This event directly associated Middle Eastern conflicts with soaring oil prices — a staggering 300% increase between October 1973 and March 1974. This surge was, in turn, connected to marked inflation and stock market declines, culminating in the early 1970s’ bear market. However, this remains the only Middle Eastern war to have had a prolonged, damaging effect on both markets and the economy.

Historically, financial markets have demonstrated a remarkable ability to weather geopolitical storms. While initial reactions to unexpected geopolitical events can be sharp, these disturbances tend to be short-lived, and markets often rebound relatively quickly post-event. This resilience underscores the idea that, in the long run, markets are more influenced by fundamentals such as economic data, corporate earnings, and monetary policy than by geopolitical disturbances.

Recently, as geopolitical tensions have ratcheted up, there has been a noticeable surge in the price of gold—a traditional safe-haven asset. Since the conflict started on October 7th, the precious metal’s price has soared by over 8.4%, reaching its highest level in the last five months. As of October 31st, gold futures were hovering just below the $2,000 per ounce mark. This significant uptick from its recent low of $1,835 in early October underscores the heightened sense of caution among investors and their search for safer assets during uncertain times.

Given the current global oil supply constraints, the U.S. had previously turned a blind eye to Iran shipping more oil, effectively sidestepping existing sanctions. However, there are now indications that the U.S. might reinforce its stance on these sanctions against Iran. Enforcing stricter measures on Iranian shipments could exacerbate the already tight oil supplies.

This strain on supplies is compounded by the U.S.’s diminished strategic petroleum reserves. Additionally, it’s unlikely that Saudi Arabia will increase its oil production amidst the ongoing conflict. As a result, even without factoring in the war premium, which could surge if a ground invasion of Gaza occurs, the price of oil is poised to remain high.

The ongoing hostilities in the Middle East have, thus far, elicited a relatively muted response from the markets. However, there remains a significant risk to these markets, particularly if the conflict expands and poses a threat of a global recession.

One of the primary economic repercussions could be an escalation in oil and gas prices, which would further exacerbate the already heightened global inflation. Additionally, there might be a decline in consumer confidence, especially in regions like the U.S. and Europe. This decline has the potential to hinder the post-pandemic economic recovery. Furthermore, in these uncertain times, the U.S. dollar might strengthen its position as a safe haven. While this could result in cheaper imports, it might also have a detrimental effect on major exporters. Lastly, there is increased uncertainty regarding how the Federal Reserve might respond to these evolving developments.

Conclusion

The first half of the year witnessed a remarkable performance in the stock market, primarily led by mega-cap technology stocks. However, a pullback ensued post-July, triggered by slowing progress on disinflation, robust economic data, and substantial U.S. government debt issuance impacting the bond market. October saw the continuation of this trend, with notable declines in both stock and bond markets. Mega-cap growth stocks showed more resilience than value stocks, attributed to their substantial cash reserves and minimal debt.

Sector-wise, Utilities and Technology sectors posted gains, while economically sensitive sectors like Energy and Consumer Discretionary saw significant declines. In the bond market, the 10-year US. Treasury yield continued its upward trajectory, affecting bond values inversely, especially for longer-term bonds. Key market drivers included rising rates, stretched valuations, a hawkish Federal Reserve, and a ballooning Federal deficit leading to extensive bond issuance.

Stock valuations appeared stretched, and the equity risk premium reached a two-decade low. The robust labor market and excess savings fueled consumer spending, with September’s retail sales report reflecting this trend. However, the robust economy risks further fueling inflation and prompting a more hawkish Federal Reserve stance.

Looking ahead, several factors could stabilize markets: interest rate adjustments, changes in U.S. Treasury bond supply, positive earnings revisions, and favorable seasonality. The Federal Reserve’s stance, geopolitical events, and the market-friendly U.S. Treasury Quarterly Refunding Announcement are crucial elements to watch. Earnings season shows positive trends, and historical data indicates favorable market performance in November and December.

Near-term market risks include escalating geopolitical tensions, especially in the Middle East, affecting oil prices, and the possibility of the Federal Reserve hiking interest rates further. The conflict between Israel and Hamas presents two scenarios: a localized conflict or a broader regional war, each with different implications for global markets and oil prices. The Federal Reserve’s warning about the global financial structure’s vulnerability to geopolitical risks highlights potential market disruptions and inflationary pressures.

Financial markets have generally shown resilience to geopolitical events, with fundamental factors like economic data and corporate earnings being more influential in the long run. The recent spike in gold prices reflects investor caution, while oil supply constraints and the Middle East conflict pose additional risks to markets, potentially leading to higher oil prices and affecting global economic recovery.

Sincerely,

The James Research Team

This material is distributed by James Investment Research, Inc. and is for information purposes only. No part of this document may be reproduced in any manner without the written permission of James Investment. It is provided with the understanding that no fiduciary relationship exists because of this report. Opinions expressed in this report are the opinions of James Investment and are subject to change without notice. James Investment assumes no liability for the interpretation or use of this report. Investment conclusions and strategies suggested in this report may not be suitable for all investors and consultation with a qualified investment advisor is recommended prior to executing any investment strategy. Past performance is not indicative of future results. All rights reserved. Copyright © 2023 James Investment.