Monthly Recap

As the economic landscape unfolded in 2024, several notable developments emerged. First, inflation moderated from s, complemented by an upswing in corporate profits. The Federal Reserve (Fed) also put an end to the current interest rate hikes and indicated the possibility of rate cuts later in the year, providing a favorable backdrop for market performance.

The S&P 500 Index surged to record highs in early January, driven by optimism surrounding a ‘soft landing’ scenario and continuing the rally from late October. This optimism was supported by various data releases affirming the resilience of the U.S. economy.

However, the S&P 500 Index closed the month on a weaker note as the Federal Reserve’s hawkish tone at the January 31, 2024 meeting rattled risk markets. The Fed signaled reluctance to cut rates in March, pushing back on market expectations. The Minutes from the January Federal Open Market Committee (FOMC) meeting leaned hawkish, with officials highlighting risks associated with moving too quickly to cut rates and acknowledging upside risks to both inflation and economic activity due to momentum in aggregate demand. Economists interpreted these minutes as affirming a timeline for the first rate cut around mid-year, aligning with market expectations for a full cut in June 2024.

Investors had been anticipating a shift at the Federal Reserve from increasing to decreasing interest rates starting in March, which initially pushed stock market indices to new highs early in the year. However, this optimism encountered a temporary setback with the release of January’s Consumer Price Index (CPI) and Producer Price Index (PPI) figures, which were slightly higher than expected, thereby reigniting concerns over inflationary pressures. These apprehensions are likely to escalate following the most recent inflation data, released on the last day of February. The Core Personal Consumption Expenditures Price Index (PCE), a crucial inflation gauge monitored by the Federal Reserve, saw its fastest rise in nearly a year in January, underscoring the central bank’s prudent approach towards lowering interest rates. The investment community keenly observed these indicators, recognizing the challenges they pose to both the economy and monetary policy.

NVIDIA & the Other Magnificent 6

In February, U.S. equity indexes experienced a remarkable surge, with the S&P 500 Index increasing by 5.17%, reaching a new all-time high. A major contributor to this surge was NVIDIA’s stellar earnings report, which exceeded Wall Street’s expectations, resulting in a significant 28.58% rise in NVIDIA’s share price throughout the month. Moreover, impressive performances by the other companies in the so-called Magnificent 7 (Amazon, Apple, Google, Meta, Microsoft, and Tesla) propelled the Bloomberg Magnificent 7 Total Return Index up by 12.06% during February. According to Bloomberg data, the average earnings per share for this group of leading tech firms soared by 55% in the fourth quarter of 2023 compared to the previous year, underlining their substantial impact on market movements.

The day after announcing its earnings, NVIDIA’s stock price surged by 16%, pushing its market value above $2 trillion. The company’s revenue for the fourth quarter tripled, and bullish forecasts for Q1 2024 further fueled investor confidence. NVIDIA’s performance not only elevated other tech stocks benefiting from Artificial Intelligence (AI) but also attracted new investors to the stock market. Investors who had allocated funds to money market accounts last year are now experiencing the Fear of Missing Out (FOMO) as they observe the surge in the Technology sector, led by NVIDIA. In 2023, $1.3 trillion was invested in U.S. money market funds, pushing their total assets to over $6 trillion.

The equity market’s uplift went beyond NVIDIA, with the S&P 500 Index and NASDAQ Composite experiencing their best performances since January 2023 and February 2023, respectively. NVIDIA’s milestone of achieving a $2 trillion market capitalization not only underscores its dominance but also highlights its valuation surpassing that of some major developed market stock indices including those of South Korea, Australia, Spain, and Sweden.

The market’s upward trajectory continued into late February, achieving new record highs despite initial challenges. This rally was characterized by broader participation across various sectors, in contrast to the dominance of the Technology and Communications sectors in previous months. All eleven sectors reported positive gains. Contrary to expectations, the top-performing sectors were not the Technology and Communications sectors, typically known for their tech-heavy stocks, but rather the Consumer Discretionary and Industrial sectors, which advanced by 7.89% and 7.18% in February, respectively. The sectors trailing behind were those more sensitive to interest rate changes, namely Real Estate and Utilities, which only saw modest increases of 2.57% and 1.06%, respectively.

Continuing the trend observed at the close of 2023, growth stocks have consistently surpassed value stocks in performance by a considerable margin in February. The stock market upward momentum was evident across the board, with both large and small stocks experiencing significant gains. Specifically, stocks within the Russell 1000 Index, representing larger companies, and those in the Russell 2000 Index, indicative of smaller firms, have excelled, recording increases of 5.40% and 5.65% in February, respectively. It is important to note that past performance is not indicative of future results.

Market Dynamics & Future Outlook

The discourse on policy adjustments, particularly the Federal Reserve’s cautious stance on interest rate cuts, has led to a recalibration of market expectations. Initially anticipated rate cuts have been scaled back, with the market now expecting fewer reductions over the year. This adjustment reflects a broader skepticism towards rapid easing by central banks, considering the economy’s resilience and ongoing inflation pressures. The yield on the 10-year U.S. Treasury bond increased from 3.88% at the beginning of February to 4.22% by month’s end. The Bloomberg U.S. Aggregate Bond Index, a comprehensive measure of the bond market, declined by 1.41%.

As we look ahead, the financial landscape remains dynamic, influenced by a mix of economic data, corporate earnings, and policy decisions. The resilience of the U.S. economy, coupled with strategic moves by the Federal Reserve, will continue to shape market trends and investor sentiment. The ability of the market to adapt and respond to these factors will be crucial in determining the trajectory of economic growth and market performance in the coming months.

Topic of the Month: Small Caps

Small cap stocks, representing companies with smaller market capitalizations, have historically commanded a premium over large caps, offering investors significant growth potential and the possibility for enhanced portfolio returns. Despite their allure, these stocks are now trading at some of their lowest valuations in years, reflecting their vulnerability to economic cycles and interest rate fluctuations. The prevailing economic environment, characterized by heightened e economic uncertainties and rising interest rates, has made smaller firms less attractive to investors.

Advantages of Investing in Small Caps

Investing in small cap stocks has traditionally been favored by those seeking higher risk along with potential rewards. Small cap stocks are often seen as engines of growth, with the potential to deliver significant returns over time. These companies, typically in their early stages of development, have ample room for expansion and innovation, which may translate into robust revenue and earnings growth. Moreover, smaller firms are frequently targeted for mergers and acquisitions by larger companies seeking to expand their market presence or acquire new technologies. This acquisition potential can drive up the value of small cap stocks, offering investors the opportunity for capital appreciation. Including small cap stocks in a diversified investment portfolio may help spread risk and potentially enhance overall returns.

Disadvantage of Investing in Small Caps

Despite their potential advantages, small cap investing comes with its own set of challenges. Small cap stocks tend to be more volatile than their larger counterparts, experiencing sharper price fluctuations in response to market sentiment, economic conditions, or company-specific news. This volatility can amplify investment risks and lead to significant short-term losses. Moreover, small cap companies are often more sensitive to changes in economic conditions, particularly during periods of economic contraction or uncertainty. Economic downturns can disproportionately impact small caps, as these companies may face challenges in accessing capital, maintaining profitability, or sustaining growth. Historically, small cap stocks typically have lower trading volumes and liquidity compared to larger, more established companies. This limited liquidity can make it difficult for investors to buy or sell shares at desired prices, potentially leading to increased transaction costs or price volatility.

Factors Contributing to Recent Underperformance

Several factors have contributed to the recent underperformance of small cap stocks. The Federal Reserve’s tightening monetary policy and successive interest rate hikes have raised borrowing costs for small cap companies, potentially squeezing profit margins and hindering growth prospects. Higher interest rates can also dampen investor sentiment towards riskier assets, including small cap stocks. Additionally, a significant portion of small cap debt is subject to floating rates and shorter maturities, making refinancing needs more pressing and adding to their vulnerability. Moreover, there has been a notable decline in the quality of small cap indices over the past two decades. With interest rates on the rise, small caps find themselves burdened with comparatively heavier debt loads, posing challenges in refinancing amidst a tightening consumer and credit environment. Twenty years ago, approximately 25% of companies in the Russell 2000 Index were unprofitable; today, that figure has increased to roughly 40%.

Additionally, the number of Russell 2000 Index non-financial companies that cannot pay their interest expenses with their operating income has increased from 314 as of December 31, 2003, to 480 today. Today, these so-called “zombie” stocks are mainly found in the Healthcare, Industrials, and Technology sectors.

Economic Uncertainty & Sector Composition

Apart from interest rate pressures, economic uncertainty and sector composition discrepancies have also weighed on small cap performance. Concerns over slowing global economic growth, inflationary pressures, and geopolitical tensions have prompted a flight to safety towards larger, more stable companies, disproportionately impacting small cap stocks. Moreover, the makeup of small cap indices, with their greater emphasis on traditional sectors such as Financials, Industrials, and Real Estate, stands in contrast to the growth-centric areas like Technology and Communication Services, which have spearheaded market gains in recent times. This discrepancy in sector focus has resulted in small caps lagging their larger cap counterparts.

Currently, Technology represents 28.75% of the large cap Russell 1000 Index but only 14.09% of the small cap Russell 2000 Index. The small cap index contains twice as many energy companies as the large cap index. Financials are the top-weighted sector in small caps, whereas Technology holds that position in large caps.

Opportunities & Risks in Today’s Market

Despite the challenges, there are opportunities for small cap investors in today’s market. As economic conditions stabilize and uncertainty diminishes, small cap stocks may experience a resurgence in investor sentiment and economic growth. While there is no guarantee for the future, small caps have historically demonstrated outperformance during periods of economic expansion, driven by their heightened sensitivity to growth prospects and earnings momentum.

With the economy showing signs of improvement, lower inflation, and the end of the Fed hiking cycle, our research suggests small caps may be poised for a rebound. Their cyclical nature, sensitivity to interest rates and the economy, and higher beta historically position them to shine in the early stages of expansion.

The Russell 2000 Index saw a boost from recent optimism surrounding peak Federal Reserve interest rates, outperforming the Russell 1000 Index. Since the market’s bottom on October 27, 2023, the Russell 2000 Index has recorded a gain of 26.18% compared to the 24.89% gain for the Russell 1000 Index. However, the Russell 2000 Index remains nearly 16% below its 2021 peak, while the Russell 1000 Index reached its all-time high on February 29, 2024. Following the Federal Reserve’s recent hawkish stance and increased discussion of “higher for longer” interest rates, the Russell 2000 Index has been underperforming its larger counterpart, underscoring small caps’ sensitivity to interest rate changes.

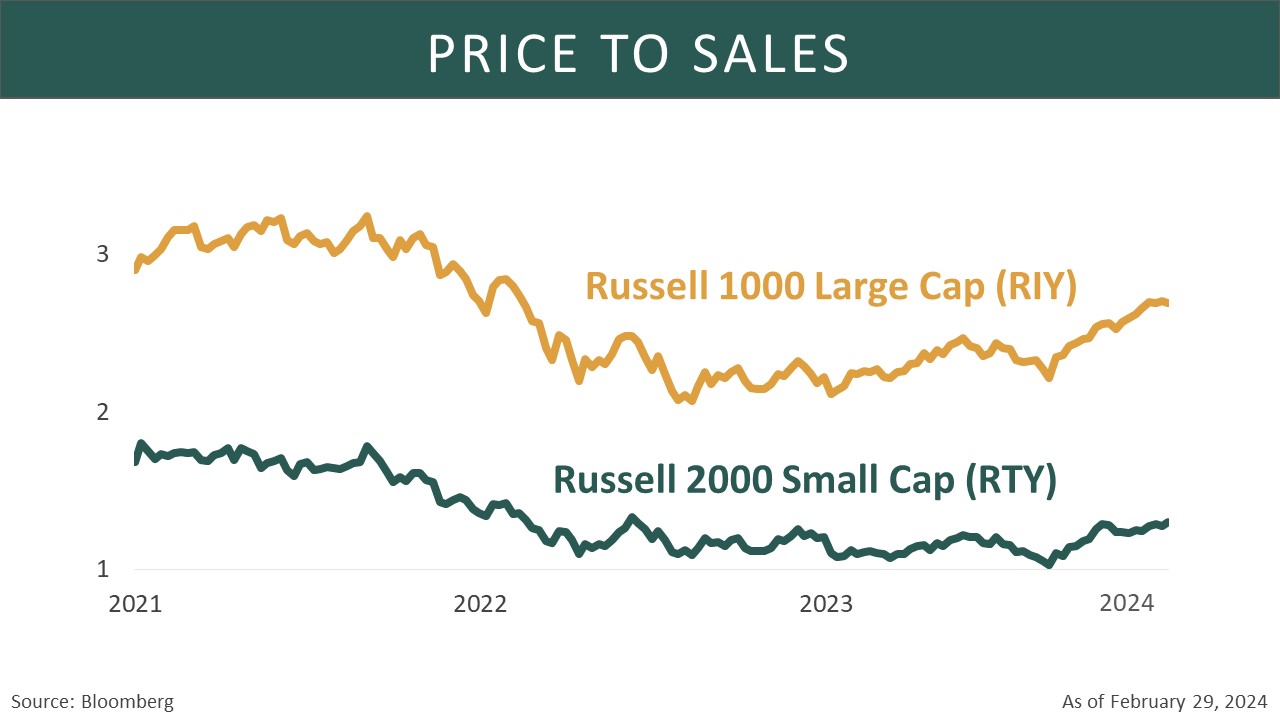

This could be the entry point for those seeking this type of risk/return scenario because stocks of small companies are currently trading at historically low valuations relative to larger ones, with the price-to-sales ratio for the Russell 1000 Index at 2.59 and 1.27 for the Russell 2000 Index.

Structural Challenges

Structural shifts in the market pose significant hurdles for small cap investors. Increased competition from private equity, regulatory obstacles for initial public offerings (IPOs), and a declining quality of small cap indices are among the challenges faced. In the present environment, substantial pools of private equity and venture capital are competing with public markets to provide equity funding to smaller enterprises. Consequently, more promising businesses are choosing to remain private or delay their IPOs due to the growing regulatory complexities within public markets. There has also been a noticeable increase in smaller companies being taken private compared to previous periods, introducing a detrimental selection bias into small cap indices. These structural headwinds may limit the potential rebound in small cap performance and necessitate a discerning approach to investing.

Active Management

Given the heightened volatility and variability of returns within the small cap universe, active management strategies may be better suited to navigate the complexities of this market segment. Active managers can utilize fundamental research, sector expertise, and risk management techniques to identify undervalued opportunities and help mitigate risks effectively.

Conclusion

In February, the financial narrative was influenced by persistent inflation, a cautious stance from the Federal Reserve, and a positive trend in corporate profits, highlighted by NVIDIA’s standout stock performance that boosted market sentiment. Despite initial challenges, including a hawkish Fed stance and inflation concerns, the S&P 500 Index and NASDAQ Index reached new highs, fueled by optimism for a ‘soft landing’ and strong economic indicators. NVIDIA’s impressive earnings not only propelled its stock and the Technology sector but also revitalized the broader market, leading to substantial gains across various sectors. The Federal Reserve’s cautious approach to rate cuts, tempering market expectations from an anticipated six to just three, reflected a cautious optimism among investors. This balance of enthusiasm with an awareness of ongoing economic and inflationary pressures exemplified the dynamic interplay between the Fed’s policy, corporate performance, and investor sentiment, highlighting the market’s adaptability in navigating uncertainties.

While the broader market, buoyed by companies like NVIDIA and optimistic economic indicators, demonstrates resilience and adaptability, the story shifts when focusing on small cap stocks. This segment, traditionally celebrated for its high growth potential and returns, is currently encountering significant headwinds. Valuations have fallen to multi-year lows, highlighting their susceptibility to economic fluctuations and shifts in interest rates. Despite these challenges, which include heightened volatility, greater economic sensitivity, and liquidity issues, small caps continue to offer the potential for significant rewards, particularly to investors who are prepared to navigate these complexities with active management. The present economic uncertainty, along with discrepancies in sector composition and structural shifts in the market, has exacerbated their underperformance. However, opportunities for a resurgence remain, especially if economic conditions begin to stabilize and the Federal Reserve starts to ease its monetary policy. The combination of Federal Reserve policies, economic growth, and the influence of artificial intelligence highlights the increasing significance of active management in leveraging the inherent growth opportunities of small-cap stocks, while also mitigating their related risks.

Sincerely,

The James Research Team

This material is distributed by James Investment Research, Inc. and is for information purposes only. No part of this document may be reproduced in any manner without the written permission of James Investment. It is provided with the understanding that no fiduciary relationship exists because of this report. Opinions expressed in this report are the opinions of James Investment and are subject to change without notice. James Investment assumes no liability for the interpretation or use of this report. Investment conclusions and strategies suggested in this report may not be suitable for all investors and consultation with a qualified investment advisor is recommended prior to executing any investment strategy. Past performance is not indicative of future results. All rights reserved. Copyright © 2023 James Investment.