Key Insights

• Disconnect between the market and Federal Reserve interest rate expectations.

• Odds of a recession remain elevated due to weakening economic data.

• Earnings deterioration is not priced in the market for 2023.

Monthly Recap

The stock markets enjoyed a nice advance for January despite the challenging year for both stocks and bonds in 2022. The month of January was a reversal of what drove the markets last year, with communication services and consumer discretionary outpacing all other sectors. These were two areas that disappointed investors in 2022. Defensive sectors were the top performers in 2022 but have been some of the biggest laggards among the S&P 500 sectors in January. Consumer Discretionary sector advanced 15.1%, and Communication Services sector rallied 14.8% and were the best two sectors in the month, while Utilities and Healthcare fell 2%, and 1.8%, respectively. Small-cap stocks rebounded and outperformed their larger brethren as the Russell 2000 Index gained 9.8%, and the S&P 500 advanced 6.3% for the month.

Last year bond investors witnessed some of the worst declines in decades, with U.S. Aggregate Bond Index down 13.0%. Fortunately, just like stocks, the bond market has enjoyed a nice rebound in January as yields have fallen and concerns about inflation eased. The U.S. Treasury market has rallied across the curve and prices have risen, especially for those on the long end. The 10-Year U.S. Treasury note yield has fallen steadily all month and is down to 3.51% from 3.88% at the end of December. The US Aggregate Bond Index rallied 3.3% in January. As bond yields fall, prices rise.

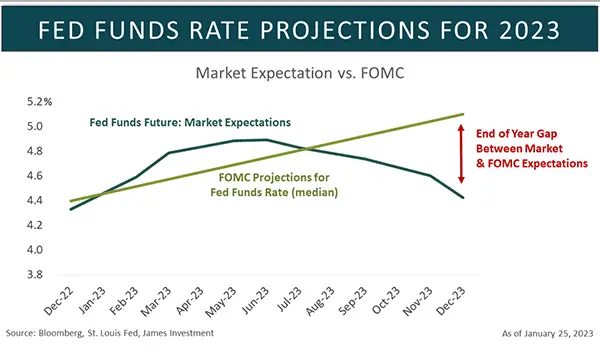

Market Interest Rate Expectations vs. The Federal Reserve Expectations

The market’s focus on inflation and rising interest rates has been the key driver of the decline in asset prices over the last 12 months. Fortunately, recent trends in inflation and the possibility of the worst being behind us are shifting market expectations. The market projects that the Fed will quit hiking in the second half of 2023, and this has shifted investor optimism as they move money to riskier assets.

Further, the latest reading on consumer prices for December turned downward and was the first monthover-month decline in consumer prices since May 2020. The expectation for easing inflation and the chance the Federal Reserve (Fed) will shift its view on rate hikes has investors optimistic in the near term. Unfortunately, the Fed continues to talk down expectations and suggests interest rate hikes might not be as aggressive, but high rates could be here for an extended period of time. As you can see, there is a disconnect between the market and Fed expectations of interest rates.

Concerns For Recession Are On The Rise

Heading into 2023, the risk of a recession was on the rise. Economists worry that economic growth is slowing along with weakened production and rising costs. The impact this could have on consumer spending could ultimately drive the U.S. economy into a recession. Recent economic data continues to trend in that direction as growth moderates and spending slows. Additionally, regional Fed reports show continued weakness, especially in manufacturing and new orders. Industrial Production, a good proxy for economic growth, also declined unexpectedly last month. All these points to weaker growth as we begin 2023.

Topic Of The Month: Earnings

Ahead of one the most anticipated recessions in history and concerns over weakening economic data, the markets are now focusing on companies’ profitability. Higher wage inflation and lower sale volume are pushing companies to lower expenses by announcing job cuts, especially in the high-tech and financial sectors. According to FactSet, analysts are now forecasting a profit recession, with two back-to-back quarters of negative earnings for the S&P 500.

While still early in the fourth quarter earnings season, the results have underwhelmed. The S&P 500 Index is reporting a year-over-year decline in earnings due to a combination of negative earnings surprises and downward revisions to earnings estimates by analysts. Only 29% of the companies in the S&P 500 have reported actual results, showing a 5.0% decline in earnings growth versus an increase of 4.3% in the third quarter. The majority of companies that have reported so far have shown earnings surprise lower than their 5- and 10-year averages.

As of January 27th, analysts are projecting a decline of 5% in earnings for the fourth quarter. These estimates are almost double the number they projected at the beginning of December. This will be the first time the S&P 500 Index has reported a year-over-year decline in earnings since the third quarter of 2020.

In the last quarter, the Energy and Industrials sectors have led the positive year-over-year earnings growth camp. Propelled by higher oil prices, the Energy sector, with its whopping 59% year-over-year earnings growth, is the most significant positive contributor to the S&P 500 fourthquarter growth. In contrast, the Materials, Consumer Discretionary, and Communication Services sectors are expected to lead the negative earnings growth group. Amazon, Alphabet, and Meta were notable decliners in their sectors.

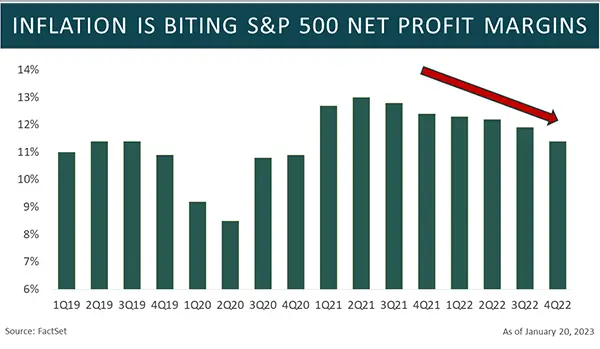

Inflation continues to worry markets; even though it has been falling from its peak of 9.1% last June, it is still elevated at 6.5% in December. Further, the Producer Price Index (PPI), a gauge for companies’ input costs, increased by 6.2% in December. The higher input costs and rising interest rates are a concern, given their negative impact on net profit margins. Profit margins are on pace to decline for the sixth quarter in a row. Additionally, while moderating, the year-over-year wage growth still stands at 6.1% for 2022, according to the Atlanta Fed Wage Growth Tracker.

Strong companies with pricing power were able to pass along these rising costs. However, as Andre Schulten, the chief financial officer of The Procter & Gamble Company, pointed out last week, “Now we’re in a tough period in terms of input costs, foreign exchange, and inflationary pressures on consumers.” In 2022, the Fed hiked faster and further than other central banks pushing the dollar to levels not seen in decades. As we saw last year, a rising dollar created headwinds for exporting companies. Recently, we have seen a weaker dollar as interest rates have moderated in the previous two months. This could provide a cushion to earnings, especially for large international companies.

2022 PE Compression and 2023 Earnings Deterioration

Last year, the equity markets began their bear market decline after a meteoric rise in valuation due to excessive government fiscal spending and the central bank’s loose monetary policy. With the benefit of hindsight, they did too much stimulus, and inflation exploded. This resulted in the Fed needing to tighten to fight decade-high inflation. This restrictive monetary policy had a negative impact on both equity and fixed-income securities. Last year’s bear market resulted in the compression of the PE ratio (priceto-earnings ratio) as the numerator (price) declined, and the denominator (earnings) remained stable. This lower valuation is promising for long-term investors and the outlook for equity markets.

2023 Analyst Earnings Expectations

Starting in 2023, we believe that most of the valuation compression is probably done, and the trajectory of equity prices will depend on what will happen to earnings in 2023. The consensus in 2023, we believe that most of the valuation compression is probably done, and the trajectory of equity prices will depend on what will happen to earnings in 2023. The consensus is for earnings to decline 3.2% in 2023, per Bloomberg estimates. However, that negative number has a bumpy trajectory. Consensus expects earnings to decline in the first and second quarters of this year by -4.9%, and -2.7%, followed by an earnings recovery of 0.1%, and 10.9% growth in the third and fourth quarters of this year.

In the markets, you outperform by assessing whether the consensus is right or wrong and acting accordingly. Hence, one needs to determine the consensus projection here. To do this, a more straightforward way of looking at earnings is to look at the trend of analyst estimates for the next 12-month earnings per share (EPS). This trend peaked in June 2020 at $230 per share for the S&P 500 Index and is now estimated to be $223 per share or a 2.7% decline in estimates per Bloomberg. Since 1950, the peak-to-trough decline in S&P 500 EPS during historical recessions is a median of 13%. So, if the already-enacted Fed tightening would lead to a recession in 2023, the earnings have further to go before we see a bottom. The likely scenario is that earnings estimates will need to be cut more.

2023 Earnings Guidance

The The term guidance is defined as a projection or estimate provided by a company ahead of reporting actual results for the quarter or the year. Negative guidance is classified as a projection by the company that is lower than average estimates. Positive guidance is a projection that is higher than the average estimate. At the time of writing, 253 companies in the S&P 500 have issued earnings guidance for the 2023 calendar year. Roughly over half of them have issued negative EPS guidance for 2023.

Conclusion

The recent disconnect between the Fed projections of interest rates and the market expectations is worrisome. Currently, in the market, there are two different views: a soft economic landing camp and a hard economic landing.

The soft-landing camp argues that inflation is coming down rapidly, and the Fed may end its hiking cycle soon and move to the sideline. A tight labor market and healthy consumer balance sheet are a tailwind of this hypothesis. In addition, declining input costs, easing supply chain issues, and faster China re-opening will help earnings growth.

The hard landing camp views the unprecedented Fed tightening, with its jumbo successive rate hikes last year, have not been reflected in the U.S. economy. The part of inflation that is most impacted by labor costs, core services, is still high and rising. This is the main reason the Fed is keeping its hawkish stance. Economic data is deteriorating, CEO confidence is low, leading indicators point to significant weakness ahead, the Fed is focused on lagging indicators, and rising geopolitical risk. Earnings estimates continue to fall as input costs continue to pressure profit margins and inflationary pressures on consumers hurt companies’ revenues.

The market is not pricing in potential earnings deterioration ahead or the rising recession risk. Furthermore, our longterm indicators remain bearish. We suggest avoiding excessive equity positioning and continue to favor quality companies with strong balance sheets and favorable pricing power. We still believe bonds should continue to play an essential part in balanced portfolios despite last year’s dismal results. Investors should begin adding longer-term bonds to their portfolios as the negative correlation between stocks and bonds likely returns.

Sincerely, The James Team