Monthly Recap

A More Accommodating Monetary Policy

Expectations of potential policy easing by the Federal Reserve (Fed), bolstered by positive economic data including tame inflation figures, a cooling labor market, and robust consumer spending, are shaping market outlooks. Against this backdrop, the Federal Reserve’s approach to rate cuts this year is increasingly apparent, but market participants are now focusing on the broader implications of this policy shift. The key question is not just when cuts will begin, but what the overall easing cycle will look like and how it will impact various asset classes.

Federal Reserve Chair Jerome Powell and colleagues have signaled a more flexible approach to policymaking, hinting a possible rate cut in September. This adaptability suggests that the Fed is prepared to respond to evolving economic conditions rather than adhering to a rigid policy framework centered almost exclusively on inflation. The positive economic indicators, particularly the moderation in inflation and a sustainable economic growth rate, have reinforced expectations of a shift towards a more accommodative monetary policy.

Despite September’s anticipated timing for the first rate cut, focus is shifting to the longer-term monetary policy outlook for 2025, which is expected to be clearer in the coming months. For investors attempting to position their portfolios medium to long term, this forward-looking perspective is crucial.

Notably, there has been a significant convergence between equity and bond markets’ expectations and the Fed’s narrative. This alignment suggests market participants have adjusted their outlooks to better match the central bank’s communicated intentions, potentially reducing the risk of sudden market dislocations due to policy surprises.

This evolving monetary policy landscape has several implications:

For equities, the prospect of lower rates typically supports valuations, particularly for growth stocks. These valuations are currently relatively high, especially for AI stocks. However, the impact may vary across sectors depending on how the broader economy responds to policy easing. The goal of continued growth while managing inflation will prove to be challenging. The effectiveness of this balancing act will be closely watched.

In the bond market, the anticipated rate cuts are likely already priced in to some extent. The focus will be on the pace and extent of the easing cycle, which will influence yield curves and fixed income strategies.

As the year progresses, market participants will be keenly analyzing economic data and Fed communications to refine their expectations of the easing cycle’s pace, magnitude, and duration. This evolving monetary policy environment will likely remain a key driver of market dynamics across asset classes in the coming months.

Market Leadership Change

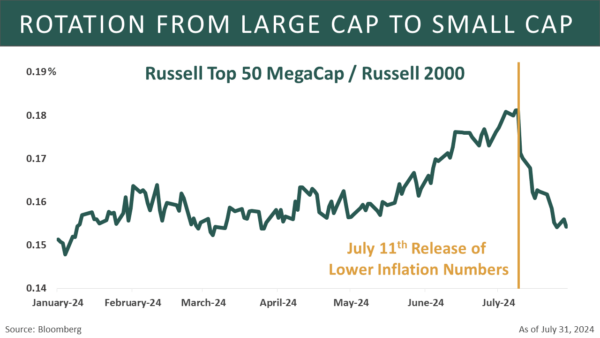

In July, the stock market experienced a significant shift in leadership, with a notable rotation away from the previously dominant Technology sector. This change was particularly evident as previously lagging cyclical sectors gained momentum, most strikingly manifested in a sharp rally of small-cap stocks.

The divergence in broader market indexes underscored this rotation. Small-cap stocks significantly outperformed their large-cap counterparts in July, with the Russell 2000 and S&P 600 indexes surging over 10%, while the large-cap S&P 500 Index eked out a mere 1.22% gain and the tech-heavy NASDAQ Index fell 1.59%.

This rotation is occurring within a complex economic landscape. The U.S. economy has shown surprising resilience, defying earlier predictions of a recession. A “soft landing” scenario, characterized by falling inflation, easing Federal Reserve policy, and sustained economic growth, have fueled investor sentiment and contributed to the shift towards more cyclical sectors.

While equities have delivered solid returns this year, it’s important to note the overall gains in the S&P 500 Index have been significantly influenced by sharp rises in the largest tech companies. The market-cap weighted nature of the S&P 500 Index means larger companies have a disproportionate influence on index moves. The average year-to-date gain for the mega-cap tech names (often referred to as the “Magnificent 7”) of 37% has been a powerful force for much of the first half of 2024, continuing a trend from 2023 when these stocks were responsible for most of the S&P 500 Index’s 26% gain.

The Russell Top 50 Index (RTOP50) includes the largest 50 securities in the Russell 3000/The Russell 2000 Index (RTY) includes the smallest 2000 securities in the Russell 3000.

The market dynamics shifted significantly in July, marking a notable change in sector performance. The S&P 500 equal-weight index substantially outperformed its market cap-weighted counterpart, posting a robust gain of 4.4% compared to the meager 1.2% increase of the market cap-weighted index. This disparity underscores broader market participation and the rotation away from the mega-cap tech stocks that had previously led the market.

Rate-sensitive sectors emerged as the top performers in July. Real Estate surged 7.2%, Utilities rose 6.8% and Financials gained 6.4%. These previously lagging sectors benefited from shifting interest rate expectations and a broadening economic outlook. Conversely, the year’s prior star performers saw a reversal of fortune, with the Technology sector declining 3.3% and Communication Services falling 0.2%.

This sector rotation reflects changing investor sentiment, potentially driven by valuation concerns in tech stocks and growing confidence in other areas of the economy. It also suggests market participants are repositioning their portfolios in anticipation of potential changes in the interest rate environment and broader economic conditions.

The shift in market leadership demonstrates the importance of diversification and highlights how quickly sentiment can change, even within a single year. However, strong fundamental support for large-cap stocks persists. Earnings expectations for large-caps have increased significantly more than those for small-caps, suggesting that the current rotation may face headwinds if it is to become a long-term trend.

Markets received additional support from the decline in bond yields during July. The yield on the 10-year Treasury note, a key benchmark for borrowing costs across the economy, experienced a significant decrease. Starting at 4.397% at the end of June, it fell to 4.04% by the close of July, representing a substantial reduction in borrowing costs.

This downward shift in yields had a positive impact on the broader bond market. The Bloomberg U.S. Aggregate Bond Index, widely regarded as a comprehensive benchmark for the overall bond market, responded favorably to this yield decline. For the month, the index posted a robust gain of 2.42%.

As the situation remains fluid, market participants should stay alert to further shifts in economic indicators, policy decisions, and political developments, all of which could influence the depth and longevity of this market rotation. Investors and analysts will be watching closely to see if this trend continues or if it represents a temporary rebalancing in an otherwise tech-dominated market.

The Artificial Intelligence Investment Boom

The extraordinary investment in artificial intelligence by U.S. technology giants is sparking both investor interest and concern. According to Arete Research, as reported by the Financial Times, AI leaders such as Amazon, Meta, Microsoft, and Alphabet are projected to spend a staggering $480 billion on capital expenditure over the next two years, primarily to construct around 100 data centers. This unprecedented scale of investment underscores the tech industry’s conviction in the transformative potential of Artificial Intelligence.

As this AI investment cycle unfolds, the market is focused on two critical questions: who will reap the most benefits from AI, and when will these massive investments yield significant returns? Analysts suggest the AI boom will likely follow a typical technology cycle, benefiting different sectors in stages:

Stage 1: Infrastructure Providers: Companies like Nvidia, producing GPUs (graphic processing units), are positioned to benefit first. Nvidia’s stock has seen significant gains year-to-date, and according to FactSet, it’s the largest contributor to earnings growth in the Information Technology sector. Without Nvidia, the sector’s estimated year-over-year earnings growth would fall from 17.2% to 7.8%.

Stage 2: Platform Companies: Next are the hyperscalers, cloud vendors such as Microsoft Azure, Google Cloud, and Amazon Web Services. These companies are building vast datacenters and are expected to continue heavy investment in GPU capacity. However, their high valuations mean they must consistently beat earnings expectations to avoid investor disappointment. Google’s recent earnings miss, for instance, spooked the AI group and the broader market. Nvidia has dropped over 10.5% from its high on June 20!

Stage 3: Application Companies: Software firms developing AI-powered applications are next in line. However, none have yet deployed products with a material impact on revenues or profits. Even highly anticipated projects like Apple’s Intelligence AI initiatives have faced delays.

Stage 4: The Wider Economy: The final stage is expected to benefit sectors like manufacturing (robotics), education, healthcare, and others through AI-driven automation and innovation.

Investors and market participants are keenly observing this unfolding cycle, looking for indicators of which companies and sectors will emerge as the biggest winners. They’re also anticipating when the financial fruits of these enormous AI investments will materialize, which could significantly impact market valuations and economic growth in the coming years. The challenge for investors lies in navigating the high expectations and valuations in the AI sector while identifying sustainable long-term opportunities across the evolving AI landscape.

Another Bright Earnings Season

The economic environment continues to be conducive to corporate earnings growth, with many companies surpassing analysts’ expectations during the first quarter earnings season. However, markets have shown unusual sensitivity to companies failing to meet estimates, closely examining whether earnings justify the significant valuation increases seen over the past six months, particularly for highly valued tech companies with strong year-to-date performance.

As we approach the midpoint of the earnings season, the outlook for earnings growth has improved significantly. According to Bloomberg, despite elevated market volatility in response to a few second-quarter reports, including those of mega-caps Tesla and Alphabet, the overall earnings season has been better than expected. This is especially true for the 493 non-“Magnificent Seven” S&P 500 members. The index is on track for more than 11% year-over-year EPS growth, and excluding the “Magnificent Seven,” it’s still pacing better than 7%, with nearly 80% of companies beating expectations.

Three of 11 sectors are expected to show earnings declines from a year ago, while Consumer Staples and Industrials are now projected to show profit growth, contrary to preseason estimates. Leading in exceeded earnings forecasts are the Financials and Healthcare sectors.

FactSet’s data corroborates this positive earnings trend. With 41% of S&P 500 companies reporting actual results for Q2 2024, 78% have reported a positive EPS surprise, and 60% have reported a positive revenue surprise. The blended year-over-year earnings growth rate for the S&P 500 is 9.8%, which, if maintained, would mark the highest year-over-year earnings growth rate since Q4 2021 (31.4%).

Earnings revisions have also been favorable. The estimated year-over-year earnings growth rate for Q2 2024 has increased from 8.9% on June 30 to the current 9.8%. Six sectors are reporting higher earnings today compared to June 30, due to upward revisions to EPS estimates and positive EPS surprises.

However, it’s important to note that valuations remain elevated. The forward 12-month Price-to Earnings (P/E) ratio for the S&P 500 stands at 20.6, which is above both the 5-year average (19.3) and the 10-year average (17.9).

This earnings season highlights the resilience of corporate America amidst economic uncertainties, while underscoring the market’s heightened scrutiny of company performances, particularly in the context of elevated valuations.

Topic of the Month: Presidential Elections

The upcoming U.S. presidential election could significantly impact various sectors of the economy and financial markets. While a Trump victory would likely yield different consequences compared to a Harris win, it’s crucial to consider the broader political landscape, including congressional control, when assessing potential outcomes.

According to pundits, a Trump presidency might bring more aggressive trade policies, including across-the-board tariffs and steeper levies on Chinese goods. This approach could benefit domestic companies but potentially harm those with high exposure to China. Less regulation under Trump could boost heavily regulated sectors like banking and energy. His immigration policies could impact the labor market, while traditional oil and gas companies might thrive under pro-oil policies. The defense sector could see increased spending, and cryptocurrencies might gain traction given Trump’s recent positive comments.

In contrast, a Harris administration would likely continue supporting renewable energy, benefiting electric vehicle manufacturers and related industries. Cannabis stocks could see growth, while pharmaceutical companies might face pressure due to drug pricing reform efforts. Banks could face tighter regulations and higher capital requirements, and there’s potential for increased corporate and wealth taxes. Harris’s approach to Chinese tariffs might be less aggressive than Trump’s

However, the composition of Congress is equally crucial in shaping economic and policy outcomes. Control of Congress is essential for passing bills and enacting legislation. Without a cooperative legislature, the policy implications of either party winning the executive branch can be significantly diminished. A unified government has a greater capacity to enact sweeping changes, while a divided government often leads to gridlock or compromise. It is interesting to note that the bond markets typically like gridlock because it puts a damper on excessive spending.

Research in behavioral finance suggests that politically biased investing can be detrimental to portfolio performance. Meir Statman, a renowned professor in this field, observes “People’s positive sentiment when their party is in power leads them to think the world will deliver higher returns with lower risks.” This cognitive bias can significantly influence investment decisions, often to the detriment of portfolio performance.

A comprehensive study conducted from 1991 through 2002, analyzing the behavior of approximately 60,000 investors, revealed that investors tend to take greater market risks when their preferred political party controls Washington. Conversely, when their party is out of power, these same investors grow restless and trade more frequently, often underperforming those whose preferred party is in charge.

These findings underscore the potential pitfalls of allowing political biases to influence investment decisions. The false sense of security when one’s party is in power can lead to overconfidence and excessive risk-taking. On the other hand, anxiety and hyperactivity when one’s party is out of power can lead to unnecessary trading and missed opportunities.

To mitigate these biases, investors should maintain a long-term perspective that transcends political cycles. It’s crucial to base investment decisions on fundamental economic and company-specific factors rather than political sentiments. Regularly rebalancing portfolios based on predetermined asset allocation strategies, seeking diverse sources of information, and considering collaboration with a financial advisor can help maintain a more rational approach to investing amidst political fluctuations.

Historically, election years have been positive for the stock market, with the S&P 500 rising in almost every election year since 1960, barring significant economic crises. The S&P 500 has advanced in more than two-thirds of the years since 1926, spanning eight Republican and eight Democratic presidencies.

In conclusion, while the presidential race garners much attention, a holistic view of the electoral landscape is crucial for anticipating potential policy shifts and their implications for the economy and financial markets. Investors should focus on long-term economic trends and company fundamentals, rather than making investment decisions based solely on political preferences or short-term market reactions to political events.

Conclusion

The current economic and financial landscape is characterized by several key factors investors should consider. The Federal Reserve is expected to transition towards a more accommodative policy, with potential rate cuts. This shift is supported by positive economic indicators, including moderate inflation and sustained consumer spending. Concurrently, a notable shift from technology sector dominance to broader market participation has been observed, with small-cap and cyclical stocks gaining momentum. This rotation reflects changing investor sentiment and expectations regarding interest rates and economic conditions.

Massive investments in artificial intelligence by tech giants are shaping the market, with potential impacts across various sectors. The AI boom is expected to benefit different industries in stages, from infrastructure providers to application companies and eventually the wider economy. Meanwhile, corporate earnings have shown resilience, with many companies surpassing expectations. This positive trend underscores the overall health of the economy, despite some market volatility.

The upcoming U.S. presidential election could significantly influence various economic sectors and market dynamics. However, investors are cautioned against making decisions based solely on political preferences, as behavioral finance research shows this can lead to suboptimal outcomes.

In light of these factors, investors are advised to maintain a long-term perspective that transcends political cycles and short-term market fluctuations. It’s crucial to base investment decisions on fundamental economic and company-specific factors, stay diversified, and regularly rebalance portfolios. Investors should remain alert to shifts in economic indicators, policy decisions, and market trends. Considering professional financial advice can help mitigate cognitive biases and emotional decision-making.

Overall, while the market presents both opportunities and challenges, a disciplined, well-informed approach to investing remains crucial for navigating the complex and evolving financial landscape. By focusing on long-term economic trends and company fundamentals, rather than short-term political or market fluctuations, investors can position themselves to capitalize on opportunities while managing risks in this dynamic environment.

Sincerely,

The James Research Team

This material is distributed by James Investment Research, Inc. and is for information purposes only. No part of this document may be reproduced in any manner without the written permission of James Investment. It is provided with the understanding that no fiduciary relationship exists because of this report. Opinions expressed in this report are the opinions of James Investment and are subject to change without notice. James Investment assumes no liability for the interpretation or use of this report. Investment conclusions and strategies suggested in this report may not be suitable for all investors and consultation with a qualified investment advisor is recommended prior to executing any investment strategy. Past performance is not indicative of future results. All rights reserved. Copyright © 2023 James Investment.