An Indepth Forecast Of The Year 2023

Second Quarter Recap

Despite the widespread pessimism pervading the financial markets, their actual performance is surprisingly robust. The first quarter of the year closed on a sour note as numerous banks required bailouts to avert defaulting on their deposits. This troubling development was succeeded by worries regarding a potential U.S. government default on its debt, owing to the constraints of the ‘debt ceiling’ mandate.

Recently, the Treasury Department announced in June that the National Debt had surpassed $32 trillion for the first time ever. This news was closely followed by the announcement that the debt ceiling had been suspended until the close of 2024. Investors seemed to take this news in stride, behaving almost as if it were a familiar scenario. After President Biden signed the legislation, investors started reintroducing riskier assets into their portfolios. This shift resulted in a rise in stock prices as they moved away from more conservative fixed income investments, leading to bonds lagging stocks.

Inflation appears to finally be trending in the right direction. The headline Consumer Price Index (CPI) figures peaked in June 2022 at 9.1%, and the most recent reading came in at 4.0%, demonstrating the substantial reduction many had hoped for. The decrease in inflation was significant enough to enable the Federal Reserve (Fed) to forego a potential rate hike at their last meeting in June 2023. At one point, markets had anticipated a pause, implying the Fed would maintain stable rates for an extended period. Now, however, this term has evolved into a ‘skip’, forecasting another rate hike as early as July of this year. Regardless of perceptions about the Fed, it can be argued that their decision to raise rates has indeed helped to curb soaring inflation, perhaps without excessively hampering the U.S. economy

Just fifteen months ago, the Federal Reserve began raising rates from their historically low level of 0.25% to their current standing, a full 500 basis points (5.0%) higher. Federal Reserve Chairman Jerome Powell and his team are striving to orchestrate a soft landing, which implies a reduction in inflation without plunging the U.S. economy into a full-blown recession. For much of 2022, this ideal scenario seemed improbable to many. However, as we move into the mid-year of 2023, the prospect of such a soft landing no longer appears as farfetched.

As we near the end of the first half of 2023, the S&P 500 Index has experienced a year-to-date increase of 16.88%. But it’s important to understand the dynamics of this surge. A significant portion of this brisk climb has been driven by the world’s largest technology stocks. In fact, the top ten stocks in the market account for two-thirds of this rally. To truly experience what many would classify as a thriving bull market, we need to see a rally from smaller stocks and a broader participation from diverse sectors.

Throughout much of the quarter, the S&P 500 Index saw a considerable rise, with gains close to 8.74%. Meanwhile, the Russell 2000 Index also advanced, albeit not as strongly, demonstrating a solid 5.19% return. However, bonds, as represented by the Core U.S. Aggregate Bond Index, didn’t fare as well, registering a decline of just under 1% over the past quarter.

Economy

Business Cycle

The economy continues to reside in the late-cycle phase of the business cycle, maintaining modest growth and staving off a recession. However, we are steadily advancing further within this late cycle, edging closer to a potential recessionary environment. Fortunately, this process has been gradual, with no anticipation of negative growth in the near term. Growth estimates for Gross Domestic Product (GDP) remain positive for the latter half of the year. Notably, the Federal Reserve is diligently striving to curb inflation by tightening monetary policy and raising interest rates, actions that could, over time, dampen economic growth.

Over the past several quarters, we’ve highlighted struggles in the manufacturing and goods sectors, while the services sector has kept the economy afloat. Additionally, the labor market has shown resilience, with new jobs being added each month. Consumer spending has been bolstered by higher wages. Although we observe a similar pattern today, there are beginning signs of strain in both the labor market and the services sector.

Labor Market

The May employment data from the U.S. Labor Department paints a mixed picture. Nonfarm payrolls added 339,000 jobs, indicative of strong increases in the labor market. However, a separate household survey showed a decline in employment, leading to an increase in the unemployment rate from 3.4% in April to 3.7% in May. The job gains in May were broad-based across sectors such as professional and business services, healthcare, government, construction, and transportation. In contrast, the technology sector has been experiencing job cuts.

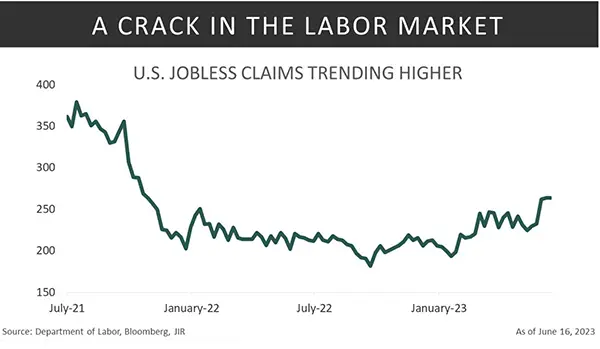

A recent shift of concern has been the uptick in initial jobless claims. Traditionally, these claims have been a key indicator of economic activity and a predictor for future changes in the labor market. The levels in late June have returned to those last seen in October 2021. This uptick might indicate that the interest rate hikes by the Federal Reserve are finally impacting the labor market. If this trend continues to rise and the levels get too elevated, it could be cause for concern. However, the recent levels have not reached those often associated with recessions.

Wage increases have remained steady, with average hourly pay rising by 4.3% compared to the previous year. An area to monitor closely is the reduction in average weekly hours worked per employee. Reduced work hours often signal impending layoffs, but employers are motivated to retain workers due to the challenges of hiring and training during the pandemic. The reduction in average work hours per week, while not alarming at current levels, could indicate an economic downturn in some sectors.

In conclusion, the U.S. job market continues to exhibit strength, but there are some signs the tide could be turning. A combination of rising unemployment, reduced work hours, and a rise in jobless claims suggest that the Federal Reserve rate hikes may be starting to affect the labor markets. However, current indicators do not suggest an imminent recession.

Manufacturing and Services

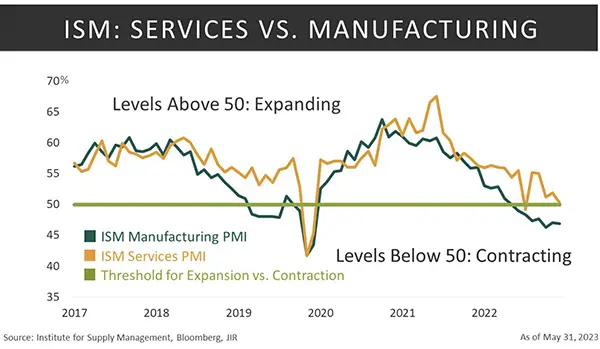

The Institute for Supply Management (ISM) manufacturing and services surveys are crucial indicators of the overall health of the U.S. economy. The manufacturing survey measures the economic activity of the manufacturing sector, gathering data from purchasing managers across various industries. This survey focuses on purchasing and supply chain activities within the manufacturing sector. Conversely, the services survey gauges economic activity within industries such as finance, transportation, healthcare, retail, and hospitality. Both surveys calculate factors like business activity, new orders, employment, supplier deliveries, and prices to provide insights into the direction the sectors are moving and whether they are growing or contracting.

As of May, this year, the two surveys have painted contrasting pictures. The Manufacturing Purchasing Managers’ Index (PMI) has contracted for seven straight months, while the Services PMI has expanded for five consecutive months. The new orders component for manufacturing continues to contract as demand eases. Growth has been difficult to find within the surveyed industries as contractions outpace growth at a ratio of 3.5 to 1. The Services PMI, on the other hand, continues to grow, with new orders also expanding at a ratio of 1.5 to 1 favoring growth.

Overall, weakness persists in the manufacturing industries, while service industries continue to expand. However, investors should note that growth in services is slowing. If the Services PMI dips below 50 and worsens, it could presage difficulties for economic growth. The most recent reading in May was 50.3.

Consumer Spending

A strong labor market and increased wages have helped boost retail spending despite rising prices. We frequently emphasize that the consumer makes up nearly two-thirds of the economy and is a key indicator for economic growth.

Today, retailers still grapple with many challenges as consumers adjust to higher prices and shift from goods to services. Despite these trends, retail sales continue to grow. According to the latest report from the Commerce Department, consumer spending increased for vehicles, restaurants, grocery stores, online retailers, and building materials. Retail sales, adjusted for seasonality, increased 0.3% in May, following a robust 0.4% growth in April.

Some reports suggest shoppers are adjusting their spending patterns to opt for products that offer better value. Despite higher prices for food and essentials, consumer spending has shown resilience and continues to contribute to the overall growth of the economy. Until consumers curb spending for extended periods, we expect growth to remain positive and a recession to be held at bay.

Housing

Housing starts experienced a significant rise in May, increasing by 21.7% to reach 1.63 million units at an annual rate — the highest level since April 2022. Both single-family and multifamily housing starts saw robust growth, with three of the four regions posting gains. Building permits also rebounded, rising 5.2%. Meanwhile, existing home sales unexpectedly rose by 0.2% in May, marking the second positive month since January 2022. A supply shortage has been a major driver in the housing market, despite higher home prices and mortgage rates.

The rise in housing starts and permits suggests that construction activity is stabilizing, reflected in 5 an increase in builder confidence. Demand remains strong as supply remains low. Despite high mortgage rates and easing home prices, the housing market may be turning the corner

Global Economy

From a global perspective, the economy is expected to slow compared to the previous year but remain positive. The World Bank forecasts a growth of 2.1% in 2023 compared to 3.1% in 2022. Concerns about inflation and global central banks tightening monetary policy are weighing on growth. Asia is predicted to experience stronger growth, lower inflation, and more accommodating policies compared to the U.S. and Europe. The U.S. dollar could experience some weakness as central banks around the world raise interest rates. However, this trend may stabilize if the U.S. Federal Reserve decides to continue raising rates through the rest of the year.

Equity

Many investors entered 2023 with a sense of caution, anticipating a looming recession. However, contrary to expectations, stocks rallied in January following a historic tax loss harvesting season in December, following a turbulent 2022 that saw substantial stock losses. The upward trend paused in February as the dominant narrative shifted to one of strong economic performance, persistent high inflation, and the necessity for the Fed to continue raising rates. Stocks also faced a challenging period in mid-March as the lag effects of rising interest rates from 2022 started to adversely impact banks’ balance sheets.

Following the collapse of three relatively sizable banks, investors sought refuge in mega cap stocks with high cash levels and robust balance sheets, and were propelled by secular trends like Artificial Intelligence (AI). The rally in stocks began to concentrate within a few mega cap stocks, which were responsible for the majority of the market’s return year-to-date. However, in early June, smaller cap and cyclical stocks began to contribute to the market’s gains. Yet, the breadth of the market remains relatively narrow, as only 29% of stocks in the S&P 500 outperformed the index’s firsthalf return of 16.88%. Nevertheless, the emerging signs of market broadening are a positive development.

In retrospect, the rally since October’s low seems justified as the economy managed to dispel fears of recession and demonstrated resilience at the beginning of the year, despite higher interest rates and a severe banking crisis. As the acclaimed economist Milton Friedman once noted, “Monetary policies work with long and variable lags.” This suggests that the impact of interest rate hikes and quantitative tightening takes time to manifest. This was particularly true in the aftermath of the unprecedented global pandemic, which prompted historical fiscal and monetary policy measures worldwide for over two years. What the stock market bears may have overlooked is that the economy began from a strong position, meaning it would take some time to witness a slowdown.

So, what’s next? There are two key factors expected to significantly impact equity markets in the coming months. First, the trajectory of inflation and the possibility of the Federal Reserve implementing additional rate hikes, and second, the corporate earnings outlook, which is being closely watched due to concerns about potential recessions.

Moderating Inflation

Inflation may continue to be more benign than anticipated due to several contributing factors. These include favorable base effects, moderating shelter inflation, and a decrease in other core service inflation components.

Favorable base effects arise when high inflation figures from last summer will soon be dropped from year-onyear calculations in upcoming inflation reports. This will naturally lower the inflation rate, irrespective of recent economic changes.

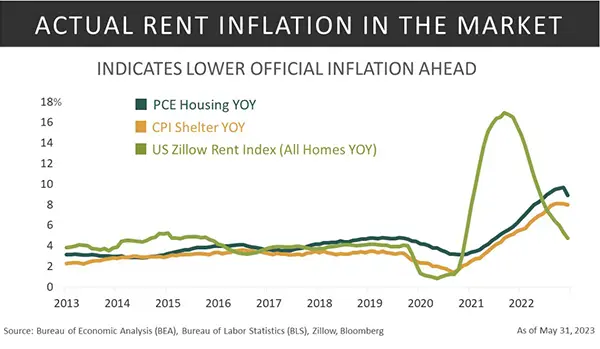

Shelter inflation, which plays a significant role in the Consumer Price Index, may be moderating as well. CPI measures are based on rental rates agreed upon six months prior. Current housing market indicators, such as the Zillow Observed Rent Index, are demonstrating a sharp year-on-year decrease in rents. This could translate into a deceleration of shelter inflation in upcoming CPI reports.

The Zillow Observed Rent Index tends to lead the official CPI shelter component and the Personal Consumption Expenditure (PCE) housing component by a period of 6 to 12 months. This means that changes in the Zillow Index can provide insights into future trends in shelter and housing inflation as measured by official CPI and PCE indicators.

Indeed, the Zillow Observed Rent Index peaked at 17% in February 2022 and has subsequently decreased to 4.8% by the end of May. This indicates that the inflation rates for shelter and housing, as measured by the official CPI and PCE indicators, likely reached their highest point in February and are expected to decline in the upcoming months.

The significance of the shelter component in inflation cannot be overstated. Shelter represents a considerable portion of the Headline CPI basket, accounting for 33%, and an even larger proportion of the Core CPI basket, making up 50%. Therefore, any progress in reducing shelter inflation has a notable impact on overall inflation.

Additionally, the high readings for food and energy inflation in 2022 are expected to diminish, leading to a subtractive effect on CPI. As these high readings roll off, they will contribute to a decrease in overall inflation numbers.

However, the situation for other core goods and services is mixed. There is a concern that goods inflation may start accelerating again, particularly if the economy surprises on the upside.

Wage growth data, as a key driver of service inflation, has shown resilience and has been a focus for the Federal Reserve. The Fed has highlighted the importance of a downward trajectory in wage growth to effectively address high inflation.

Taking a comprehensive view, we anticipate inflation will persistently deliver downward surprises, potentially reaching the 3% level during the summer. Nevertheless, vigilance is crucial for detecting any resurgence in inflation tied to an economic re-acceleration later in the year. It should be noted, however, that this scenario does not form the basis of our primary forecast.

Earnings Estimates Bottoming

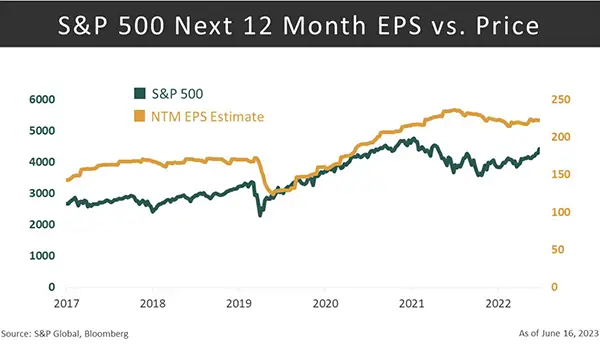

In the first quarter, earnings for the S&P 500 showed a decline of 2% compared to the same period last year. However, this result was better than anticipated, as analysts had estimated a more significant decline of 6.7% before the actual earnings reports were released. Moreover, the beat rate, which measures the percentage of companies surpassing earnings estimates, was strong, with 79% of companies outperforming expectations. It should be noted, though, that the bar was set lower leading up to the earnings season, which may have contributed to the higher beat rate.

Looking ahead, analysts predict that the second quarter will see an earnings decline of 6.4%, according to FactSet. However, they project that this will mark the bottom in the earnings growth profile and anticipate a subsequent recovery in earnings growth. In fact, the next 12-month earnings per share (EPS) for the S&P 500 is trending higher after experiencing a steady decline over the past nine months.

Given the economic challenges on the horizon, we maintain our belief that 2024 earnings estimates are overly optimistic. Analysts are currently predicting a significant jump of 12.3% in earnings growth for next year, following a modest 1.1% growth projection for this calendar year. This sharp increase in estimates appears optimistic considering the prevailing economic conditions, such as a slowing economy, declining consumption, and corporate spending, and diminishing pricing power.

In our assessment, while we view 2024 earnings estimates as still being on the high side, we do not anticipate a collapse in these estimates either. Our projections indicate a sluggish growth trajectory rather than a recessionary environment. Overall, we expect a moderate recovery in earnings growth, considering the prevailing economic factors and challenges faced by businesses.

Fixed Income

At its June meeting, the Federal Reserve maintained the official federal funds target rate steady between 5.00% and 5.25%. According to the “dot plot,” which depicts individual policymakers’ rate predictions, this decision is more of a temporary “skip” than a permanent “pause.” This interrupts a sequence of 10 consecutive rate hike meetings. Even though the Federal Reserve has decided to keep the federal funds rate unchanged for now, its subsequent hawkish communication indicates potential for further tightening in the months ahead.

Factors such as the sustained economic strength, diminished risks from a banking sector crisis, resolution of debt ceiling uncertainties, and persistent high core inflation have led the Fed to indicate that additional policy tightening may be required. This hawkish stance is reflected in the mid-range prediction for the year-end Federal Reserve funds rate, which has risen from 5.1% in March to 5.6%, implying an additional two quarter-point hikes before the end of the year.

Despite the Fed’s efforts to curb economic growth and inflation over the past 15 months, the economy continues to exhibit remarkable resilience. Even amid a slowdown in consumer spending and more moderate wage increases, companies remain committed to hiring. Given the robust state of the economy, inflation remains elevated, even with a slowdown in the overall increase of prices when excluding volatile commodities such as fuel and groceries.

The Fed has yet to embrace the narrative of peak inflation. While inflation figures have improved, they remain notably above the Fed’s target rate of 2%. The Fed’s preferred inflation gauge, the PCE has decreased from 7.0% year-over-year in June of the previous year to 3.8% this past May.

The better-than-expected inflation numbers continue to have a positive impact on both the bond and stock markets. Nevertheless, it is unlikely that the Fed will be swayed by a single monthly positive number. We should anticipate the Fed’s ongoing aggressive rate hiking campaign as long as inflation remains above its target.

The Fed is taking a measured approach, carefully increasing rates while incorporating additional data into their decision-making process. This approach is aimed at balancing the requirements of controlling inflation and avoiding an unnecessary economic downturn. A failure to swiftly control inflation could lead consumers and businesses to anticipate persistent price hikes, adjusting their behavior accordingly and further entrenching inflation.

The Federal Reserve Bank’s unexpectedly robust hawkish stance, coupled with the potential for a higher terminal rate and investors’ anticipation of a pause, has escalated bond market volatility. The gap between short- and long-term U.S. government borrowing costs has surged to its highest level since the banking crisis in March. Notably, the yield on twoyear Treasuries now exceeds that of the 10-year yield by over 100 basis points. This situation, often referred to as an inverted yield curve, typically foreshadows a recession and has now reached a level unseen in the past four decades.

This inversion typically occurs when investors expect that higher interest rates will stifle economic growth. This anticipation leads them to favor the longer end of the market. In turn, it’s likely to increase the demand for Treasuries as a safe-haven investment. Bank of America reports that investors are exhibiting greater confidence in U.S. 30-year bonds now than they did during the height of the 2008 financial crisis.

The Fed is anticipated to raise the interest rate by 25 basis points in its July 25-26 meeting, and barring a significant drop in inflation, we could foresee an additional 25 basis points increase before the close of the year.

Simultaneously, the supply of Treasury securities is expected to grow. Bloomberg reports that an influx of new Treasury bills will hit the market in the coming months. This is designed to replenish the Treasury General Account (TGA) following the debt-ceiling agreement, setting the stage for a rise in longer-term debt sales which could further inflate bond yields. Starting from August, the sale of government notes and bonds is projected to experience a surge, with the net new issuance expected to exceed $1 trillion in 2023, and potentially double in 2024 due to a widening deficit.

This expanding mix of debt issuances, coupled with the Federal Reserve’s ongoing reduction of its balance sheet, is likely to drive borrowing costs upwards. This effect is anticipated to be particularly pronounced as foreign buyers of Treasuries are deterred by the escalating costs of currency hedging.

Will these escalating borrowing costs drive the economy toward a hard landing, thereby sparking rallies in both treasuries and duration? Conversely, can a robust labor market and a resilient consumer guide us toward a softer landing, keeping the bond market largely unchanged?

Based on our analysis of the current data, we anticipate a more gradual economic slowdown, suggesting a potential for a softer landing.

Conclusion

Despite the signs of late cycle growth and the odds of a recession around the corner, there are reasons for optimism about the current state of the economy. The labor market has remained resilient, with consistent job gains and steady wage increases, although some cracks are beginning to show. While there has been an uptick in initial jobless claims and a reduction in the average weekly hours worked per employee, these levels have not reached the thresholds associated with recessions.

Furthermore, consumer spending has remained positive, supported by a strong labor market, and increased wages, even in the face of higher prices. The housing market has also shown signs of stabilization, with significant growth in housing starts and permits, despite supply shortages and higher mortgage rates. Although the manufacturing sector has contracted for several months, the service sector continues to expand, albeit at a slower pace.

Overall, while there are challenges and potential risks on the horizon, the current state of the economy suggests a cautious approach rather than an impending downturn.

The equity market has shown resilience since October 2022, despite slow, yet persistent, economic growth and continually lower-than-expected inflation. This robustness in the stock rally is justified as fears of an imminent recession were premature. The concentration of the rally is also reasonable given the defensive nature of owning mega cap technology stocks with robust balance sheets and the potential for growth from emerging secular trends, such as Artificial Intelligence.

We advise maintaining vigilance in monitoring inflation, particularly rent and wage inflation, which are the main factors influencing the Fed’s concern with core inflation. Additionally, it’s essential to keep an eye on initial jobless claims, as they provide an early indicator of potential labor market issues – a level of 300,000 claims is seen as a signal of recession.

As the economy experiences only a modest growth and core inflation persists, many bond investors find themselves in a state of cautious observation, uncertain whether interest rates will continue to stay elevated for an extended period. In such an environment, we recommend staying with high-quality bonds.

For Investors:

Economy

―The economy remains in the late-cycle phase of the business cycle, with modest growth and no immediate signs of a recession.

―The labor market demonstrates strength with job additions, but jobless claims suggest possible strain. ―While the manufacturing sector struggles, the services sector has been expanding, though the growth rate is slowing.

―Despite higher prices, consumer spending remains resilient, driven by wage growth and strong labor markets.

―Expectations are for a deceleration in the global economy relative to the previous year due to the impact of restrictive monetary policies implemented by central banks.

Stocks

―Moderating inflation in the second half is a tailwind for stocks.

―Earnings estimates are recovering for the 2nd half but are still high for 2024.

―A resilient residential housing market is keeping home prices elevated. – A tailwind to the consumer wealth effect.

―There is now a competing alternative to stocks; higher bond yields.

―The inclusion of cyclical stocks and small caps may add to market returns.

― Potential Chinese stimulus is good for emerging markets.

Fixed Income

―The Fed paused its ten-rate hike series, hinting at possible future increases owing to ongoing economic robustness and high inflation

―Despite the Fed’s tightening policies, the U.S. economy remains resilient with robust hiring, and moderate wage increases.

―Although inflation has improved, it still remains above the Fed’s target rate of 2%, keeping more interest hikes on the table.

―An increase in Treasury securities supply and the Fed’s shrinking balance sheet are headwinds for liquidity.

―Amid increasing borrowing costs and a widening deficit, we anticipate a gradual economic slowdown, pointing to a potential soft landing rather than a hard landing in the economy.

―Historically, Treasury and long-term bonds tend to do well at the end of an interest rate hiking cycle.