An Indepth Forecast Of The Year 2024

First Quarter Recap

The stock market’s record-breaking performance in the first quarter of 2024 has been driven by a combination of factors, including the anticipation of the Federal Reserve (Fed) cutting interest rates and the financial market’s strong embrace of the artificial intelligence (AI) secular growth theme. This momentum is further bolstered by a resilient economy, robust corporate earnings, and significant revenue growth.

Navigating a delicate balance, the Federal Reserve aims to control inflation while maintaining economic growth. Although the Fed has indicated that it expects to cut rates by three-quarters of a percentage point this year, it also projects core inflation — the price increase of goods excluding food and energy — to remain at 2.6% in 2024, slightly higher than its stated goal of 2%. This suggests that the path to a soft landing may be more complicated than initially thought. The Fed’s actions have significant implications for the stock market. Typically, lower interest rates are seen as beneficial for stocks, as they make borrowing more affordable and can stimulate economic activity. However, if inflation remains stubbornly high, the Fed may be forced to keep rates elevated or even raise them further, which could put pressure on stock valuations.

The concept of a “soft landing” refers to a scenario where the Federal Reserve successfully brings down inflation to its target level without triggering a recession. This is the ideal outcome that many investors are hoping for, as it would allow the economy to continue growing while keeping price pressures in check. Achieving a soft landing is a delicate task, as the Fed must carefully calibrate its policies to avoid overtightening and stifling economic activity. The current strength of the labor market and the resilience of consumer spending provide some cushion against a potential downturn in the economy. If the Fed can engineer a soft landing, it would bode well for the stock market, as it would support continued earnings growth, keeping valuations in check. Conversely, if inflation proves more persistent than expected or if the Fed is forced to take more aggressive action, it could introduce volatility and uncertainty into the market.

Nonetheless, the market’s upward trend may persist even without aggressive rate cuts from the Fed, underpinned by the solid foundations of the economy and corporate performance. Companies have shown remarkable adaptability and success in challenging conditions, with many surpassing earnings and revenue expectations. This corporate resilience instills investor confidence in the market’s capacity to navigate potential challenges. Moreover, the prospect of ongoing economic expansion, supported by historically low unemployment rates and consistent consumer spending, fuels optimism that the economy can maintain growth even with the Fed opting for a higher for longer interest rate policy.

A significant driver of the stock market’s recent stellar performance is the rapid advancement of artificial intelligence (AI) and its potential to transform various industries. The excitement around AI has been particularly evident in the information technology sector, with companies specializing in AI semi-conductor chipmaking, like Nvidia, seeing their stock prices soar. As more businesses adopt AI and machine learning technologies to enhance productivity, streamline operations, and develop innovative products and services, the technology sector could see significant growth and profitability. The impact of AI on the broader market is also noteworthy. As AI becomes more integrated into different sectors, it could lead to increased efficiency, cost savings, and new revenue streams, boosting corporate earnings and driving stock prices higher. Moreover, the disruptive nature of AI could create new investment opportunities as emerging companies and industries gain traction.

However, it is essential to recognize that the AI boom also carries certain risks. The rapid growth and high valuations of AI-related stocks have raised concerns about potential overvaluation and market frothiness. If the actual adoption and impact of AI fall short of the market’s lofty expectations, it could lead to a correction in stock prices. Additionally, the regulatory landscape surrounding AI is still evolving, and there may be unforeseen challenges or limitations that could affect the growth trajectory of AI-driven businesses. Investors should remain vigilant and carefully assess the long-term viability and competitive advantages of individual companies rather than getting swept up in the overall AI hype.

Despite concerns about high interest rates and inflation, many companies have been able to maintain profitability and even exceed expectations. The S&P 500 Index, a benchmark for the broader stock market, has seen companies collectively beat earnings expectations by 7% in Q4 2023. This positive surprise has been driven by sectors such as and communication services, which have performed well despite the challenging economic environment. These strong corporate earnings and revenue growth have been another driver of the stock market’s momentum.

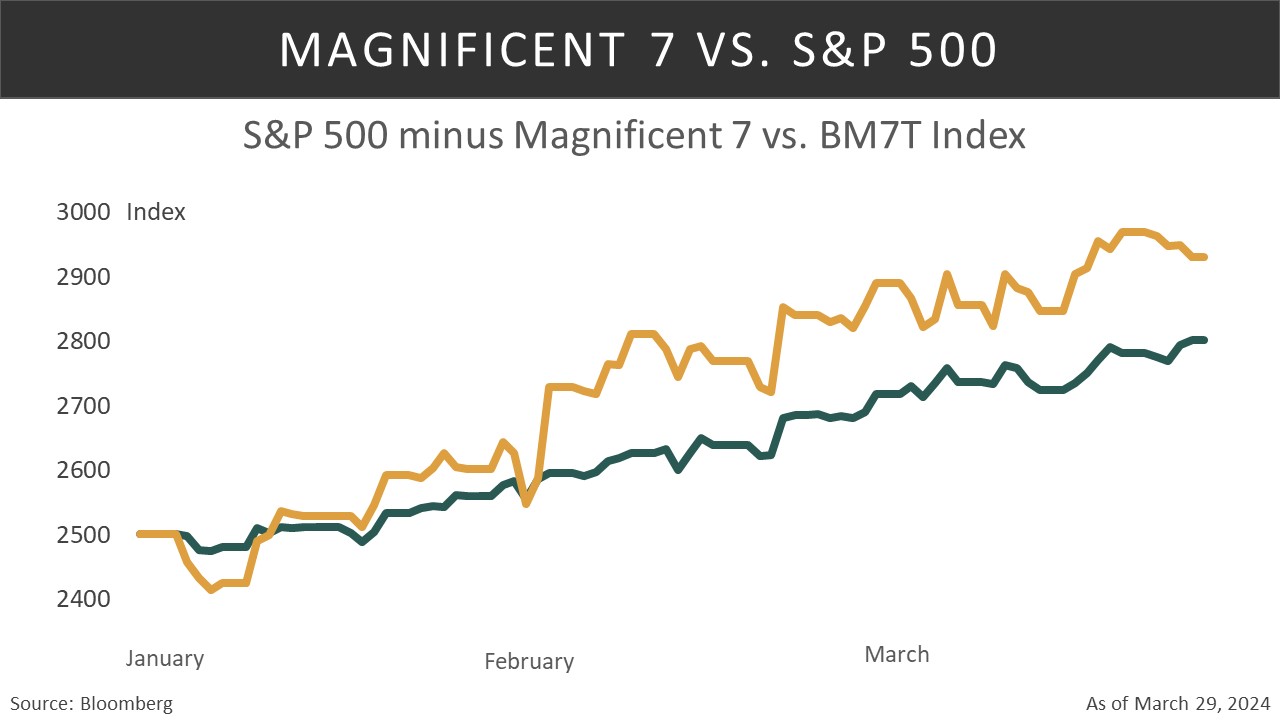

Since the beginning of the year, the S&P 500 cap-weighted Index has climbed 10.55%, surpassing the 7.91% increase of its equal-weight counterpart. This discrepancy is largely due to the outsized influence of several mega-cap companies. Notably, NVIDIA, a leader in AI, has surged by 82.46% year-to-date. Similarly, standout performances by other members of the so-called Magnificent 7 (Amazon, Apple, Google, Meta, Microsoft, and Tesla) have driven the Bloomberg Magnificent 7 Total Return Index up by 17.14% over the same timeframe, even though Tesla and Apple have experienced negative returns year-to-date. However, a broadening of the market is taking shape, with the equal-weight index and value-style investments taking the lead in March. This shift could signal a transition away from the dominant performance of the largest tech companies towards a more diversified market movement.

Since hitting its low on October 27, 2023, the S&P 500 Index has surged by more than 28%.

Every sector gained except for real estate, with cyclicals such as financials, energy, and industrials rising over 10%. The communication sector saw the greatest increase, propelled by Meta and Google, which together represent more than 46% of the sector’s weight. On the other hand, utilities, consumer discretionary, and real estate sectors underperformed. Additionally, large-cap stocks significantly outpaced small-cap stocks. Growth stocks outperformed value stocks, and gold also saw significant gains.

The U.S. Aggregate Bond Index has declined by 0.78% year-to-date, influenced by the increase in the 10-year US Treasury note rate from 3.88% at last year’s end to 4.201% by the end of March. This reflects the typical inverse relationship between bond yields and prices. During this period, corporate bonds have outperformed their Treasury counterparts, although these rates rose also.

Economy

In our Outlook for 2024 from a quarter ago, the labor market was displaying signs of loosening while staying robust overall. The labor market was fueling consumer spending and appeared to be helping the economy avoid any slowdown and a possible recession.

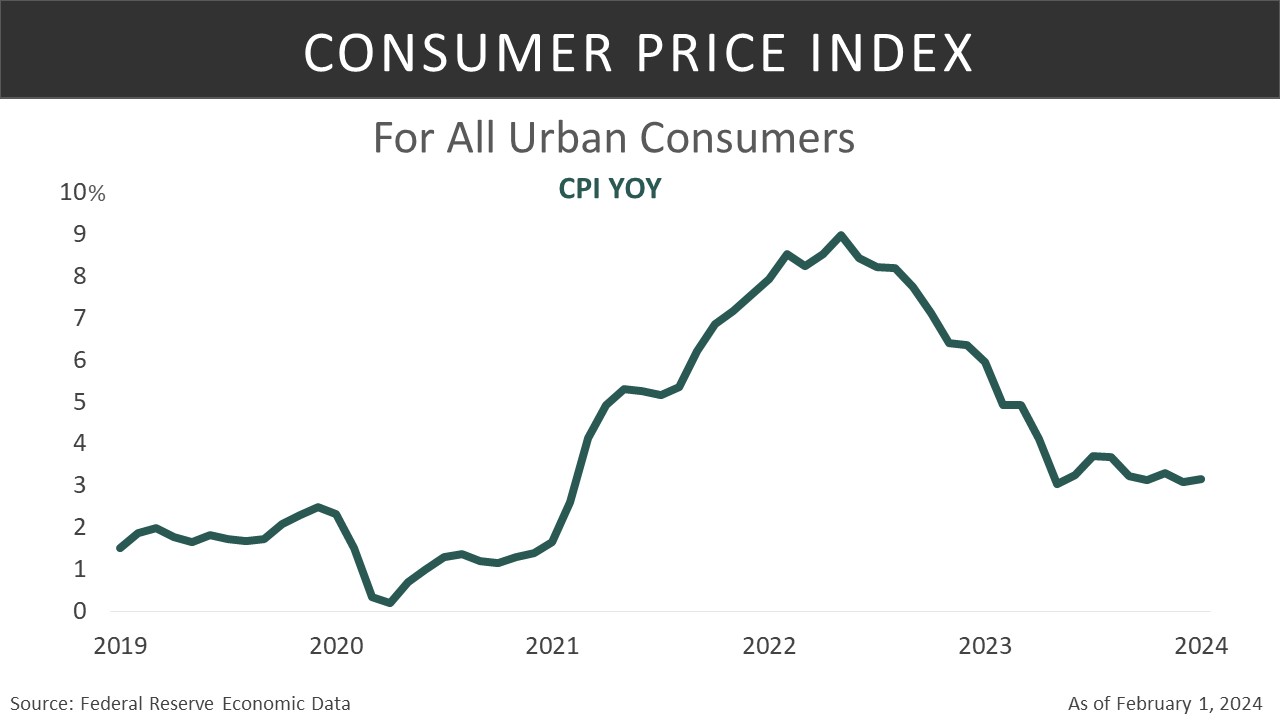

Additionally, we noted U.S. inflation dropped from its peak of 9.1% in June of 2022, with the headline Consumer Price Index (CPI) continuing to trend lower from a year ago. The trends in the data augur a potential decline to 2% inflation by the end of 2024. Our Outlook suggested inflation will likely continue to moderate, due to disinflation in housing and declining core goods. Ultimately, this would give the Federal Reserve room to implement rate cuts in 2024.

The outlook for the consumer remained positive despite a reduction in consumer excess savings. Growing wages, a strong labor market, and costs trending lower would help consumers remain resilient in 2024. Overall spending growth would be modest despite signs of some consumers actually reducing spending.

Labor Market

In recent months, we have seen several reports offering insights into the U.S. labor market which continue to show few signs of slowing down. The labor market serves as an indicator of economic health providing insights into employment, wages, and consumer confidence.

First, the year began with a wave of optimism and a surge in new jobs created in the first couple of months of the year. Further, the 3-month average for non-farm payrolls has steadily increased over the past several months and is trending higher. The unemployment rate is also holding steady and is still below 4% for the second consecutive year.

Last quarter (Q4 2023) we emphasized the steady rise in continuing jobless claims in the past several months. This trend pointed to the struggles the unemployed had in finding new jobs as the pace of hiring slowed from prior periods. Fortunately, we have seen the numbers shift gears, improving over this quarter. The latest reports show a decline of about 6% from the recent high in November 2023; a welcome sign that the health and resilience of the labor market remains strong.

Nevertheless, there have been some signs of a loosening labor market as labor demand and supply continue to stabilize. The Job Openings and Labor Turnover Survey (JOLTS) points to a softening in the demand for labor as the total number of job openings decline. The ratio of job openings to the number of unemployed available to fill those jobs is well off the high as the number of job openings has fallen nearly 3.3 million since its .

One area of concern we are watching is the number of temporary workers in the workforce. Often a decline in temporary workers precedes recessions and is a leading indicator for the labor market and economy. These jobs are often easier to cut and are let go first before full-time employees. The recent trend has been downward, which suggests the soft-landing narrative might be harder to achieve than many suggest. We will be watching this important indicator in the quarters ahead.

Inflation

Today, we note a shaky start to inflation in 2024. Previously, we highlighted the downward trend in inflation over the past year. However, the recent readings for January and February of 2024 suggest inflation might be “stickier” as it appears to be leveling off. February’s inflation, which was higher than expected for the second consecutive month, signals potential challenges ahead. With the Consumer Price Index (CPI) up 3.2% from a year ago, slightly exceeding economists’ estimates and the Fed’s target, concerns are mounting in the markets. This uptick in consumer prices, especially when coupled with rising oil and commodity prices, could lead to increased production costs for manufacturers, which ultimately would put a strain on consumers’ wallets.

Consumer prices are not our only concern as we have also seen a rise in producer prices over the same period. The latest reading for the Producer Price Index (PPI) rose in February and was the largest increase in six months, driven by fuel and food costs. This is an important number to watch as it helps to gauge the PCE (Personal Consumption Expenditure), the preferred inflation measure of the Federal Reserve. In February, the PCE Price Index climbed by 0.3%, slightly below economists’ expectations. Core prices, excluding volatile food and energy, rose by 2.8% year-on-year, in line with forecasts.

The recent stabilization of inflation at a higher rate may shift the Fed to hold interest rates higher for longer than the markets appear to have priced in at this time. The goal of hitting a target rate of inflation of 2% may be more difficult than expected and could take longer to achieve. This is reflected by a shift in market expectations regarding interest rate cuts. Our latest outlook points to rate cuts getting pushed further out into the year, or even the possibility the Fed may need to hold rates where they are for the rest of 2024.

Breakeven Rates

Further evidence of market expectations shifting lies within the inflation breakeven levels. The breakeven rate of inflation can be calculated by taking the yield difference between a nominal Treasury bond (which doesn’t adjust for inflation) and an inflation-protected Treasury bond (which adjusts for inflation) of the same maturity.

Investors, central banks, and economists monitor breakeven rates as they provide insights into inflation expectations. The breakeven rate can show what investors expect inflation to be over a certain period based on whether the breakeven rate is higher or lower than current inflation levels. These expectations can influence investment decisions, monetary policy, economic forecasts, and consumer spending habits. For instance, central banks might adjust their monetary policy based on whether market expectations of inflation line up with their targets.

The first three months of the year have seen a dramatic shift in breakeven rates. In fact, since the start of the year the annual inflation expectation for the next 12 months has increased to 3.96%, up from about 2%. The last time the breakeven increased this fast over a three-month period, the CPI year-over-year was running over 8%. The correlation between the two is not perfect but it does lead us to believe the Fed may hold rates longer than many expect.

GDP Growth & Consumer

The first quarter of 2024 is seeing slightly stronger economic growth, with Gross Domestic Product (GDP) estimates surpassing earlier expectations. Forecasts for real GDP growth have risen from 1.3% at the end of 2023 to 2.2% today, reflected by a broad-based increase in consumption, government spending, investment, and trade. This surge in growth has led to the lowest odds of a recession in nearly two years.

The shift in growth is further highlighted by the findings from the CFO Survey, a survey from Duke University and the Federal Reserve Banks of Richmond and Atlanta. CFOs have revised their growth outlook to 2.2% over the next four quarters, up by 0.5%, and have increased capital expenditures for future projects. However, they do note some concerns about persistent price pressure and inflationary risks.

The Conference Board Consumer Confidence Index dipped slightly and reached a four-month low in March, despite the strong return in the stock market and stabilizing interest rates. People are growing increasingly concerned with how the upcoming election will affect us politically and economically. We expect consumer confidence to remain relatively steady until the next election as that becomes the forefront of consumer’s minds.

Additionally, we’ve seen a slight decrease in the overall health of the consumers despite the resilience in the labor market and slightly stronger growth, the assessment of consumers’ financial situation for the next six months has declined as consumers are becoming more worried about their financial futures. Consumers have also been more pessimistic about business conditions, income, and the labor market in the short-term.

Further, credit card use is on the rise as consumers are looking at other ways to spend and consume. In January, consumer credit increased at a seasonally adjusted rate of 4.7%, which was nearly double expectations. Furthermore, we’ve seen an increase in Buy Now Pay Later (BNPL), which is difficult to track as it is not reported to credit bureaus. The increase in consumers using BNPL in contrast to credit could show some unanticipated changes in consumer spending in the future. Unfortunately, this type of spending in the long-run is not sustainable, nor is it healthy for the overall economy.

Equity

A Stellar Earnings Season

FactSet reports that during the fourth quarter of 2023, an impressive 73% of S&P 500 companies surpassed expectations for earnings per share (EPS), while 64% exceeded revenue projections. This strong performance has not only bolstered corporate confidence but also signaled favorable growth prospects for the year ahead.

According to Bloomberg, S&P 500 Index earnings in the fourth quarter outperformed expectations, recording an 8.2% year-over-year increase compared to the projected 1.2% gain. Revenues also exceeded predictions by 134 basis points, achieving 4.1% growth. When excluding the underperforming energy sector, the Index’s earnings growth was even more remarkable at 11.9%, significantly higher than the anticipated 4.5%, while sales grew by 5.5%, surpassing the 3.9% projection. Although these robust results led to a slight downward revision in growth estimates for the upcoming quarters, the outlook remains optimistic.

The substantial earnings beat provided a boost to analysts’ confidence, marking a shift from recent quarters where strong performance often led to lowered future estimates. Bloomberg reports that the expected earnings growth for the next three quarters averages 7.4%, only slightly lower than early January projections. The positive revisions in earnings forecasts and the market’s strong response to upward guidance revisions, with companies that increased their forecasts experiencing significant single-day returns, indicate renewed investor optimism and a reassessment of future growth potential.

Moreover, there are indications that operating and net-income margins, which have faced challenges over the past two years, may be stabilizing, with some sectors even showing margin expansion. The technology and utilities sectors led this improvement, contributing to a brighter overall outlook for margins in 2024.

Shift In Corporate Sentiment

Alongside financial performance, corporate sentiment is improving, with CEOs focusing more on growth through capital expenditure and increasing investor returns through buybacks. Bloomberg’s analysis of Q4 2023 earnings conference calls for S&P 500 companies reveals that optimism has risen among America’s largest corporations, reflecting diminishing concerns over macroeconomic risks. Despite rising interest rates, financing costs have not emerged as a significant concern, and enthusiasm for capital expenditure has reached its highest point in nearly three years, paralleling discussions on buybacks and artificial intelligence.

Over the past year, the focus of earnings discussions has shifted away from previously dominant issues like recession, labor, and inflation. Instead, there has been a renewed emphasis on supply chain dynamics for the first time in a year, highlighted in the fourth quarter reports. Although conflicts in the Red Sea have impacted shipping, this has led to increased dialogue on supply chain matters, though these mentions have not surpassed levels seen in 2021.

The backdrop of easing macroeconomic concerns, such as recession, labor, and inflation fears, alongside stable financing costs despite higher interest rates, underpins this optimism. This environment, combined with the high rate of companies reporting positive surprises in earnings and revenue, underscores a resilient and potentially growth-oriented period ahead for the S&P 500 Index.

Despite market concerns about a potential economic slowdown or recession, FactSet’s analysis of conference call transcripts revealed that fewer S&P 500 companies mentioned the term “recession” during their fourth quarter earnings calls than might be expected. Only 47 companies referenced “recession,” a figure significantly lower than the five-year average of 85 and the ten-year average of 61. This marks the lowest incidence of the term’s use since Q4 2021, showing a steady quarter-over-quarter decline in mentions since the peak in Q2 2022.

The decline in recession mentions suggests a shift in corporate sentiment or market conditions, with the Financial and Industrial sectors being the most vocal about recession concerns in their recent calls. However, the relatively low overall number indicates a more optimistic outlook among the majority of S&P 500 companies compared to recent years. Furthermore, the term “soft landing” saw its highest mention in at least three years during the fourth quarter calls, with 37 companies using the term. This suggests a growing sentiment among these companies that, despite slowdown concerns, there might be a way to navigate potential economic downturns with minimal negative impact, indicating a cautious yet hopeful outlook for the economy.

High Valuations Concerns

The stock market’s strong performance in early 2024 has raised concerns about potentially inflated stock valuations and overheated trading activities. Price gains have been robust, but earnings growth has not kept pace, resulting in higher valuations and sparking worries that the market might be overvalued and susceptible to corrections. The significant influence of the “Magnificent 7” companies on market performance further compounds these concerns.

Investors and analysts use various metrics to assess whether the market or individual stocks are overvalued, fairly valued, or undervalued, with the price/earnings (P/E) ratio being a widely used tool. FactSet reports that the S&P 500 Index’s forward 12-month P/E ratio stands at 20.9, exceeding both the 5-year average of 19.1 and the 10-year average of 17.7. This ratio also surpasses the 19.5 P/E ratio recorded on December 31, 2023. Since then, the Index’s price has risen by 10%, while the forward 12-month earnings per share (EPS) estimate has increased by 2.9%.

Despite the elevated valuations, some analysts argue that the current economic conditions, such as declining inflation, a resilient U.S. economy, anticipated easing of monetary policy by the Federal Reserve, and the exit from an earnings recession, may justify these higher valuations. They suggest that even if stocks are expensive, the prices might be warranted.

Not all analysts view the elevated valuations as a cause for concern, with some arguing that the market can sustain these levels or even rise further, cautioning against missing out on potential gains due to overvaluation fears. Recent analyses by strategists from Bank of America and Goldman Sachs indicate that the current rally may have a stronger foundation than past periods of high valuation, particularly because today’s elevated valuations are concentrated among a few large growth stocks with solid fundamentals.

Nevertheless, investors should be mindful of the risks associated with high valuations, such as the comparative attractiveness of bonds due to higher interest rates, and the importance of earnings growth in maintaining market momentum. Investors are advised to consider valuation signals for identifying investment opportunities while being aware of the longer-term implications of current market valuations.

Fixed Income

Following a robust end to 2023, fixed income securities experienced a slight slowdown in the Q1 2024. Paradoxically, the underwhelming performance this year was largely a result of the significant gains witnessed in the final months of the previous year. The December 2023 bond rally led to a repricing of these investments, temporarily placing them at lower yields and higher prices, creating a challenging starting point for the new year. Although there has been a modest pullback in bonds, one thing has become evident: the Federal Reserve has concluded its interest rate hiking cycle.

Barring any significant unforeseen events, the Federal Reserve appears to have halted its rate hike campaign and has now entered a wait-and-see approach, with Fed Chair Powell suggesting rate cuts sometime this year. Although the Fed’s next move will likely be to lower the Federal Funds Rate, all signs suggest that they require additional data confirming that inflation is moderating sufficiently to prevent a surprising resurgence.

In Q1 2024, the 10-year Treasury total return index declined by 1.72%, while the more price-sensitive 30-year Treasury saw a more pronounced drop of 4.24%.

Federal Reserve Outlook

As the March 20, 2024, Federal Reserve meeting approached, the likelihood of a rate hike was extremely low, and the chances of a rate cut were slim. The Fed’s actions were largely in line with market expectations, as they chose to maintain the status quo. The Federal Open Market Committee (FOMC) kept their target rate unchanged at 5.25% to 5.50%, with a unanimous vote. The Fed members also reiterated their belief in the strength of the economy and the robustness of job growth.

The key takeaway from the meeting was the Fed’s projections for the remainder of the year, which indicated three potential rate cuts of 25 basis points each. This aspect of the dot plot, a chart that records each Fed official’s projection for the central bank’s key short-term interest rate, was sufficient to keep bond investors satisfied, as it signaled lower rates in the future. However, the plotting itself was slightly less dovish than anticipated, as the median dot remained unchanged, while the surrounding dots shifted slightly upwards.

While the outlook for the remainder of 2024 was positive for bond investors, some may have overlooked the Fed’s projections for rates in 2025 and 2026. The expectations for rate cuts in the longer term are anticipated to be less aggressive, with potentially one fewer rate cut in both 2025 and 2026 compared to previous projections.

The slight changes in the Fed’s projections can be attributed to updates in their economic and inflation forecasts. For instance, just three months ago, the Fed anticipated the economy would grow at a rate of 1.4% for 2024. However, at the most recent meeting, this projection was revised upwards to 2.1%. Similarly, the unemployment rate estimate was adjusted downwards from 4.1% to 4.0%, indicating a stronger labor market. The Fed also revised their expectations for Core PCE, a measure of inflation. Three months ago, it was believed that PCE would moderate to 2.4%, but at the recent meeting, the Fed concluded that inflation might be somewhat more persistent, remaining at 2.6% for the remainder of the year.

Despite these adjustments, several questions remain unanswered, such as when the Fed will cut rates, by how much, and for how long. However, we believe that rates are most likely to trend downwards over the long term. Consequently, bonds are currently more attractive, especially compared to the past few years when rates were on an upward trajectory.

Implications & Geopolitical Factors

While the Federal Reserve plays a significant role in the bond market, it is essential to recognize that it does not provide a complete picture. One additional positive factor for the bond market is the geopolitical events occurring worldwide. Although these events are tragic and not something we hope for, it is important to acknowledge that historically, wars have often been beneficial for bonds. The uncertainty brought about by conflict and the resulting desire for safe investments can lead to strong performance in the bond market during such times. Unfortunately, we find ourselves in this type of global environment.

The ongoing Russian war against Ukraine continues to rage on, and the re-election for Putin will only strengthen his stance. Similarly, the fighting in the Middle East persists. We note that the U.S. Treasury bond market is often seen by foreign investors as a safe haven in difficult times.

Closer to home, the rising polarization in the public discourse will likely intensify as we approach the November Presidential election. The more contentious the lead-up to the election and the greater the uncertainty that builds, the more favorable the scenario becomes for high quality fixed income investments.

With interest rates at some of their highest levels in the past decade, investors may find themselves content with adopting a buy-and-hold strategy. Treasury notes and bonds currently offer yields ranging from 4.25% to 5.0%, which may satisfy buyers who are happy to sit back, collect coupon payments, and earn income.

Quality corporate bonds are even more attractive, despite having slightly lower spreads – the difference between yields on U.S. Treasury and Corporate bonds – compared to historical levels. The additional yield offered by these bonds, coupled with a low probability of default, may be precisely what investors are seeking in the current market environment.

A bond rated BBB is recognized as Investment Grade, marking it as the lowest tier within this classification. The potential to earn over 1% more annually over Treasury bonds, whether adopting a buy-and-hold or a hold-to-maturity approach, renders these bonds attractive.

Inflation & Rate Cuts Timing Concerns

One lingering area of concern is inflation, which has proven to be more persistent than many experts anticipated. Core CPI, which excludes food and energy prices, rose 0.4% on a month-over-month basis, leaving it at 3.8% for the past year. Producer prices also came in “hotter” than expected this past month and year.

These elevated inflation readings are sufficient to give pause and question whether significant rate cuts can actually occur this year. With the Fed likely to wait and see if inflation subsides, these delays are pushing closer to the election. Historically, the Fed has been reluctant to take action in the meetings immediately preceding an election to avoid the appearance of political motivation or taking sides. For the Fed to cut rates three times, they would potentially need to do so in June or August, with one cut right before the election and another in mid-December. This timing may not be feasible if the Fed chooses to adhere to its typical behavior of avoiding rate changes close to elections.

Conclusion

The stock market’s record-breaking performance in Q1 2024 has been driven by multiple factors, including the prospect of Federal Reserve rate cuts, the transformative potential of AI, a resilient economy, and strong corporate earnings. While there are reasons for optimism, investors should also be aware of the risks and uncertainties associated with the Fed’s balancing act on inflation and the rapid growth of AI-related investments.

The U.S. economy in Q1 2024 has shown signs of resilience and growth, driven by a strong labor market, increasing consumer spending, and rising GDP estimates. However, concerns about persistent inflation, the potential impact of the upcoming election, and shifts in consumer credit behavior suggest that challenges lie ahead.

The labor market remains robust, with steady job growth and low unemployment rates, although some indicators, such as declining temporary workers and a softening in job openings, point to potential weaknesses. Inflation has proven to be more persistent than anticipated, with recent upticks in consumer and producer prices raising concerns about the Federal Reserve’s ability to reach its 2% target.

Shifting inflation expectations, as evidenced by rising breakeven rates, suggest that the Fed may need to hold rates steady for longer than initially expected. While GDP growth estimates have improved and the odds of a recession have decreased, consumer confidence has dipped slightly, and concerns about the political and economic impact of the upcoming election are growing.

As consumers increasingly turn to credit cards and Buy Now Pay Later (BNPL) options to support their spending, the sustainability of this behavior remains uncertain. The overall health of the U.S. economy in the coming months will largely depend on the resilience of the labor market, the persistence of inflation, and the ability of consumers to maintain their spending power in the face of potential headwinds.

The strong earnings season in Q4 2023 and the shift in corporate sentiment have contributed to a more optimistic outlook for the S&P 500 in 2024. Companies have surpassed EPS and revenue expectations, and there is a renewed focus on growth through capital expenditure and investor returns via buybacks. However, concerns about potentially inflated stock valuations, particularly among the “Magnificent 7” tech companies, have been raised. Investors should balance optimism with the potential risks posed by elevated valuations and the importance of earnings growth in maintaining market momentum.

The bond market in Q1 2024 has been influenced by the Federal Reserve’s monetary policy, economic indicators, geopolitical events, and inflation concerns. Despite the slight slowdown following the strong performance in late 2023, the Fed’s decision to halt its rate hike campaign and pivot towards future rate cuts have created a more favorable environment for fixed income investments. Investors may find attractive returns in Treasury notes and bonds, as well as quality corporate bonds. However, the persistence of inflation and geopolitical factors may impact the timing and magnitude of future rate cuts. A buy-and-hold strategy or a focus on investment-grade bonds may prove to be prudent approaches for investors seeking stable returns and protection against market volatility.

To conclude, the current economic environment appears favorable for both stocks and bonds. The prospect of continued earnings growth suggests that stocks may continue to trend higher throughout the year. Meanwhile, bond yields have reached levels that provide attractive returns for investors seeking stability and income, marking a significant shift from the past few decades.

However, it is crucial to keep the fundamental principles of investing in mind. Geopolitical risks remain a significant factor, and election years have the potential to introduce volatility and uncertainty into the markets. Moreover, while the outlook for stocks is bright, valuations are not particularly inexpensive.

In light of these considerations, it is advisable for investors to maintain a well-diversified portfolio. By spreading investments across various asset classes and sectors, investors can potentially mitigate risk while positioning themselves to benefit from the opportunities present in both the stock and bond markets.

For Investors:

Economy

- Labor Market Resilience: U.S. labor market remains strong, driving consumer spending and economic stability with unemployment staying below 4%.

- Inflation Trends: Inflation decreases, with a potential drop to 2% by end of 2024, suggesting room for Federal Reserve rate cuts.

- Consumer Outlook: Despite reduced savings, strong wages and a healthy labor market support continued consumer spending.

- Sticky Inflation in Early 2024: Early 2024 inflation levels challenge Federal Reserve targets, potentially dampening consumer spending.

- Fed Policy and Market Expectations: Higher-than-expected inflation rates may keep Federal Reserve interest rates elevated longer than the market expects.

- Breakeven Rates Shift: Rising consumer and market inflation expectations create headwinds for Federal Reserve rate cuts.

- Economic Growth and Consumer Sentiment: Strong GDP growth contrasts with dipping consumer confidence due to future economic and political uncertainties.

- Credit and BNPL Use: Rising credit card and Buy Now Pay Later (BNPL) usage indicate shifts in consumer spending habits, causing sustainability concerns.

Equities

- Stellar Earnings Season: 73% of S&P 500 companies beat EPS forecasts and 64% exceeded revenue expectations in Q4 2023, indicating strong growth prospects.

- Earnings and Revenue Growth: S&P 500 earnings rose 8.2% year-over-year in Q4, with revenues up 4.1%, outperforming expectations and driving optimism.

- Corporate Sentiment Improving: CEOs show growing optimism, focusing on growth, capital expenditure, and buybacks, reflecting lesser macroeconomic concerns.

- Shift in Earnings Discussions: Recent earnings calls highlight supply chain dynamics over previous concerns like recession, labor, and inflation.

- Reduced Recession Mentions: Fewer companies mentioned “recession” in Q4 2023 earnings calls, signaling a more optimistic corporate outlook.

- High Valuations Concern: Early 2024’s stock market surge raises concerns about high stock valuations, with the S&P 500’s P/E ratio exceeding historical averages.

- Economic Conditions vs. Valuations: Some analysts argue current economic improvements justify the market’s high valuations, suggesting sustained or increasing stock prices.

- Investor Caution Advised: Despite some confidence in current valuations, investors should be wary of potential stock market corrections and assess long-term implications of Federal Reserve actions, 2024 presidential elections, and consumer debt levels.

Fixed Income

- Fixed Income Slowdown: After strong gains in late 2023, fixed income securities pulled back slightly in early 2024 due to higher prices and lower yields.

- Federal Reserve Halts Hikes: The Fed has ended its interest rate increases, shifted to a wait-and-see approach, and hinted rate cuts later in the year.

- Treasury Performance: The 10-year Treasury yield index fell by 1.72%, and the 30-year Treasury dropped by 4.24% in Q1 2024.

- Fed’s March Meeting: The Federal Open Market Committee maintained rates at 5.25% to 5.50%, projecting three rate cuts of 25 basis points each for the rest of the year, but still wants to see inflation falling towards its target of 2%.

- Long-term Rate Outlook: Fed projections for 2025 and 2026 anticipate less aggressive rate cuts, reflecting updated economic and inflation forecasts.

- Geopolitical Factors: Global conflicts and domestic political polarization, particularly with the upcoming Presidential election raise market risks and volatility, which favors high quality fixed income investments over stocks.

- Investment Strategy: High Treasury yields and attractive corporate bond spreads present a compelling case for a buy-and-hold strategy in the current market.

- Inflation and Rate Cuts Concerns: Persistent inflation raises doubts about the feasibility of significant rate cuts, especially with the Fed’s cautious approach ahead of elections. This could lead to market disappointment (corrections) for both stocks and bonds.

Disclosure

This information is of a general nature and does not constitute financial advice. It does not take into account your individual financial situation, objectives or needs, and should not be relied upon as a substitute for financial or other professional advice to assess, among other things, whether any such information is appropriate for you and/or applicable to your particular circumstances. In addition, this does not constitute an offer to sell, or the solicitation of an offer to buy, any financial product, service or program. The information contained herein is based on public information we believe to be reliable, but its accuracy is not guaranteed.

Investing involves risks, including loss of principal.

Past performance is no guarantee of future results.

Definitions

Growth: A company stock that tends to increase in capital value rather than yield high income.

Value: A value stock is a security trading at a lower price than what the company’s performance may otherwise indicate.

Federal (FED) Funds Rate: the target interest rate set by the Federal Open Market Committee (FOMC) at which commercial banks borrow and lend their excess reserves to each other overnight.

Price/Earnings Ratio: ratio for valuing a company that measures its current share price relative to its earnings per share (EPS).

*Consumer Price Index (CPI): an index of the variation in prices paid by typical consumers for retail goods and other items.

*U.S. Aggregate Bond Index: designed to measure the performance of publicly issued US dollar denominated investment-grade debt.

*S&P 500 Index: S&P (Standard & Poor’s) 500 Index is a market-capitalization-weighted index of the 500 largest US publicly traded companies.

*Indexes are not managed. One cannot invest directly in an index.