An Indepth Forecast of the Year 2025

2024 Market Recap

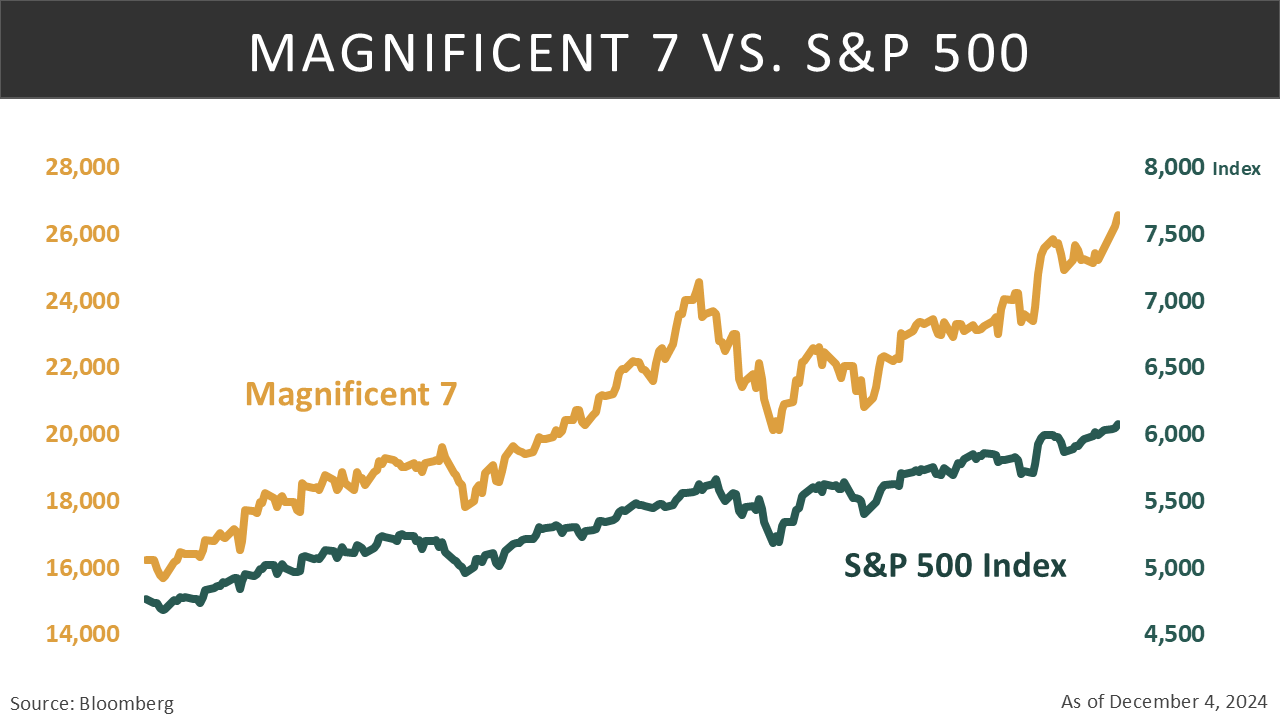

The stock market demonstrated remarkable strength throughout 2024, achieving multiple record highs and establishing a two-year bull market run. From its October 2022 low, the S&P 500 Index surged approximately 73.23%, including an impressive year-to-date return of 27.33% as of November 29, 2024. U.S. stocks attracted unprecedented investor confidence, pulling in over $1 trillion since 2020, with a record $141 billion in just the past four weeks. The “Magnificent Seven” – Apple, Amazon, Google, Meta, Microsoft, Nvidia, and Tesla – technology giants played a pivotal role in this rally, surging 55.21% while the remaining 493 stocks in the S&P 500 Index returned just 23.47%, highlighting the extraordinary influence of these mega-cap tech companies on overall market performance.

Artificial Intelligence (AI) emerged as a dominant market theme in 2024, driving strong returns across various sectors. Nvidia, at the forefront of AI chip development, saw its stock soar 173% by November 29, 2024. The AI boom’s impact extended beyond traditional tech companies, with Vistra Corp (VST), a utility company powering AI data centers, leading the S&P 500 Index with a remarkable 304.32% gain through November. The convergence of tech performance between the Nasdaq 100 Index and S&P 500 Index (both up over 20%) indicated broader technology adoption across sectors.

Magnificent 7 vs. S&P Index

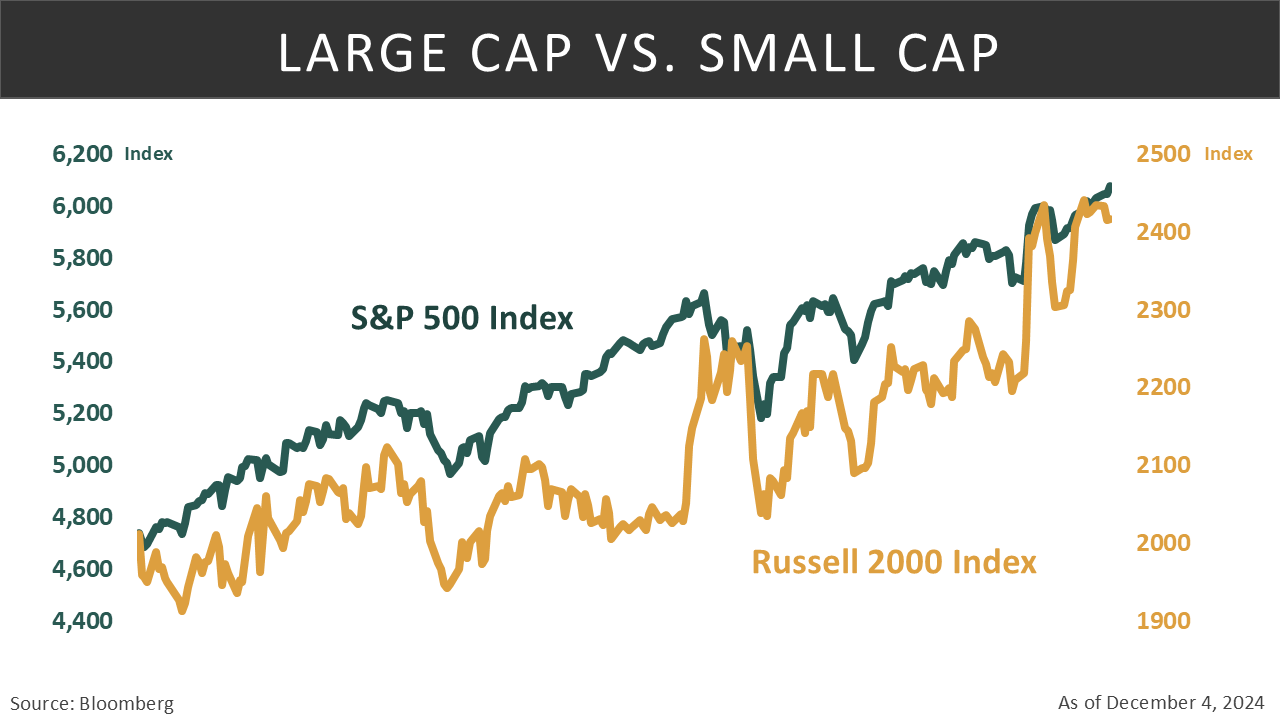

Growth stocks dominated the market throughout 2024, with the Russell 3000 Growth Index surging 30.81% compared to the Russell 3000 Value Index 22.20% return. The market showed remarkable stability with only one notable pullback in August that remained under the 10% correction threshold, indicating strong structural support and investor conviction. While large-cap tech stocks led the market’s early gains, market participation broadened in the second half of the year. Small-cap stocks, however, underperformed their larger peers, with the Russell 2000 Index returning a modest 21.23% amid concerns about economic growth and higher interest rates.

Large Cap vs Small cap (S&P 500 vs Russell 2000)

Sector performance varied widely, with all sectors posting gains by November 29, 2024. The Financials sector led with a 38.01% return, followed closely by Communication Services at 34.92%. U.S. market outperformance was particularly notable against global peers, with the Stoxx Europe 600 Index experiencing one of its worst years versus the S&P 500 Index. In contrast to the strong equity performance, bond returns remained muted, with the Bloomberg Aggregate Bond Index yielding just 2.57%. Meanwhile, Bitcoin surged following Trump’s victory, driven by his pro-cryptocurrency stance and campaign promises, while gold demonstrated resilient performance with a 27.78% return, reflecting some investors’ desire for safe-haven assets amidst economic uncertainties.

Corporate earnings exceeded expectations throughout 2024, marking the fifth consecutive quarter of year-over-year earnings growth for stocks in the S&P 500 Index, with a blended growth rate of 5.4% in Q3. The welcome decrease in inflation throughout 2024 while maintaining robust economic growth created an ideal “Goldilocks” scenario that supported equity valuations. However, market valuations have stretched well beyond historical norms. Current price levels reflect exceptionally rosy expectations that may prove unrealistic when compared to typical long-term averages and fundamentals.

The Federal Reserve’s (Fed) pivot toward monetary easing emerged as a key market catalyst in 2024. Following the end of its tightening campaign in late 2023, the Fed managed market expectations carefully throughout the year. While investors initially anticipated aggressive rate cuts, the central bank maintained a measured approach due to above-target inflation and robust labor market conditions. The Fed’s first rate cut in September 2024, a 50 basis-point reduction to 4.75%-5%, marked a significant policy shift, though market expectations gradually adjusted to a slower, more deliberate easing cycle by October.

Markets demonstrated unprecedented resilience to multiple significant geopolitical risks – Middle East conflicts, Ukraine war, U.S. elections, and Chinese economic challenges – suggesting strong underlying fundamentals. Donald Trump’s return to the White House, accompanied by a Republican-controlled Congress, triggered significant market reactions. Equity markets posted record rallies as investors anticipated the implications of potential policy changes, including tax cuts, deregulation, and shifts in trade policies. However, this optimism was tempered by concerns over increased deficits and the possibility of aggressive tariffs, particularly on Chinese imports.

Economy

The U.S. economy shows resilience amid various challenges heading into 2025. While labor markets remain stable and manufacturing sees targeted growth in key sectors, uncertainties around trade policy and monetary conditions create a complex economic landscape.

Labor Market

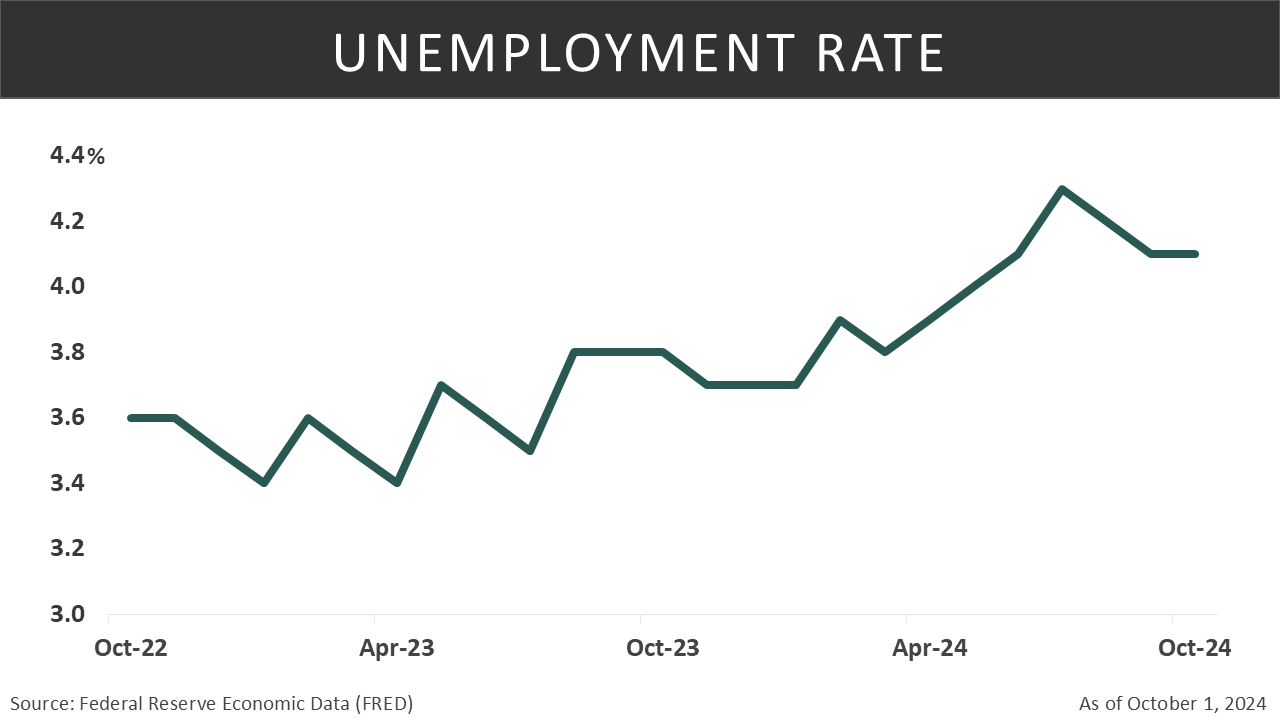

The U.S. labor market continues to demonstrate resilience as unemployment claims remain historically low, and the unemployment rate is steady at 4.1%. Wage growth remains positive, with real wages increasing across several demographics, particularly benefiting low-wage income workers. Technological advancements and Artificial Intelligence (AI) investments are driving job growth and highlight an area of future potential. Other areas such as healthcare and government have also added to job creation over the past year.

Despite its strengths, the U.S. labor market faces several challenges. Job growth has slowed significantly, with projections of further deceleration in 2025. Year-over-year growth for nonfarm payrolls shows the slowest 12-month job growth since before the pandemic. The growth in AI is promising but it could also displace workers as structural shifts occur in the labor markets and companies adjust their labor force. Temporary job losses and weak participation rates and slower hiring highlight underlying weaknesses, and headwinds as we begin a new year.

Looking into 2025, the uncertainty surrounding potential tariffs adds complexity to the labor market outlook. Tariffs could disrupt global supply chains, raise costs for businesses and limit the capacity for firms to hire. Industries dependent on international trade, such as manufacturing and agriculture, are particularly at risk. Tariffs may lead to short-term job losses in affected sectors and could impact longer-term structural changes as businesses adapt to higher operational costs. The uncertainty could reduce employer confidence, potentially slowing job creation and wage growth for affected industries.

Manufacturing

Manufacturing has shown modest growth in recent years, with Industrial Production up only 0.6% annually over the last three years – significantly below its historical average of 2.7% since 1950. Additionally, the Institute of Supply Management (ISM) Manufacturing Purchasing Managers Index (PMI) remains in contraction territory, recording its seventh consecutive month of decline in October 2024. Weak capital investments, trade policy uncertainties, and manufacturing job losses continue to weigh on the sector. New orders, a measure of future demand, remain sluggish and have been persistently weak, adding to the already constrained sector.

Heading into 2025 the potential policy changes following the 2024 U.S. elections and global geopolitical uncertainties are additional headwinds for the sector. The potential tariffs discussed could have a dramatic impact on supply chains, demand, and long-term investment in manufacturing. The industry is likely to focus on reshoring or nearshoring to improve supply chains. The impact is still uncertain, but we suspect there will be winners in some industries and losers in others as trade wars unfold.

The U.S. manufacturing sector is undergoing a historic surge in factory construction, fueled by strong private investments and policies like the CHIPS Act and a surge in datacenter investment. Additionally, the shift towards automation and investment in AI should help to improve efficiency and competitiveness in the long-term. Lower interest rates are anticipated to fuel investment and increase demand for manufactured goods.

Consumer

The full extent to which the proposed tariffs by President Trump might affect consumer behavior remains unclear. The tariffs will likely lead to cuts on personal Federal income tax, which will benefit consumer spending. Additionally, the cost of the proposed tariffs may trickle down to the consumer, resulting in higher prices. An increase in prices may lead to lower-income consumers being pressured to prioritize essentials over discretionary purchases.

Despite pressures from the proposed tariffs, consumer sentiment continues to strengthen, now 41% greater than the trough in June 2022. This rise in sentiment is anticipated to encourage more consumer spending. Additionally, any further cuts to the Fed rate will boost consumer demand. Spending has remained high even though sentiment is low, indicating consumer resilience and the ability to maintain spending despite higher costs. Savings have been reduced during 2024, with the personal savings rate in October at 4.4%, the lowest since December 2022. A reduction in savings aligns with the idea that consumers are becoming more optimistic for the near future.

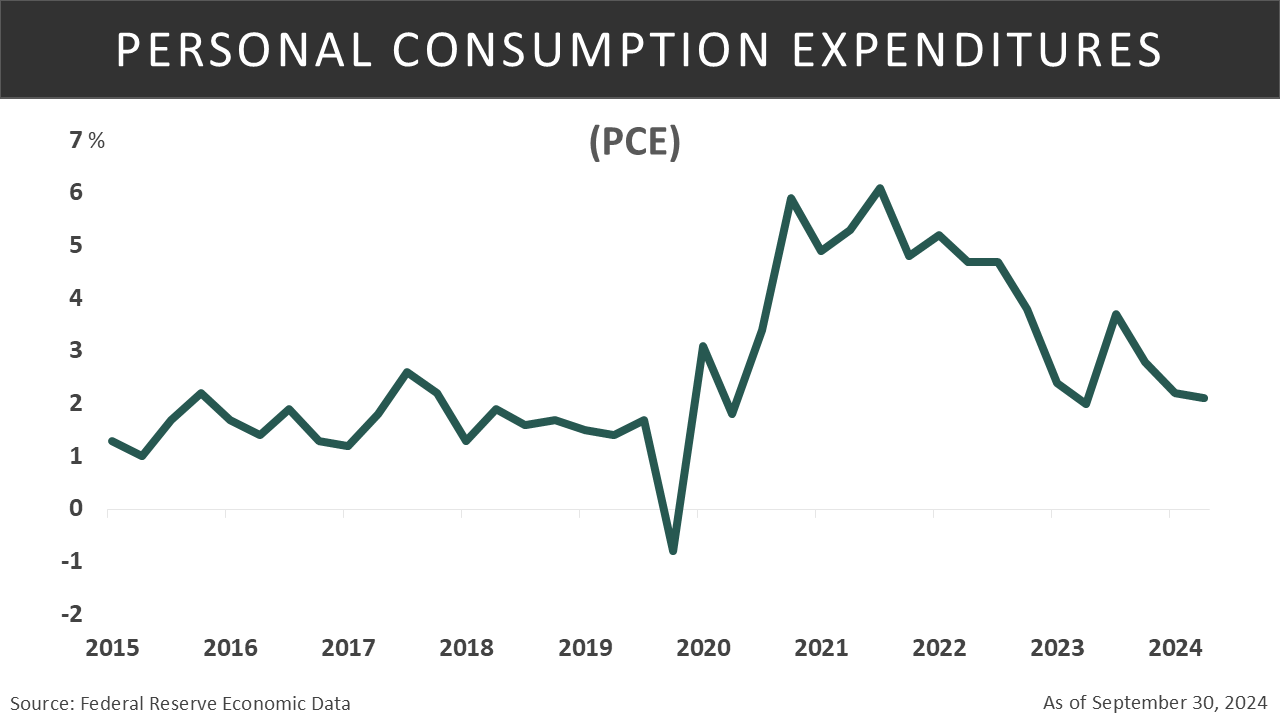

Growth in services remains robust, with 4.67% growth since January. In contrast, growth in goods has been slow, growing 2.87% this year. Retail sales have increased 2.9% from January to September, after no growth in 2023. The percentage of sales that occur online has risen, with 16.2% of total sales happening online, similar to levels seen at the height of Covid. Consumers have continued to shift to normal spending habits, as Core Personal Consumption Expenditures (PCE), which excludes food and energy, have decreased since the end of 2022 while PCE has increased year-over-year since November 2020.

Housing

Demand for homes remains strong as the supply of homes on the market remains low, driving home prices higher. Housing starts peaked in April 2022 and have since declined to pre-pandemic levels. Privately owned housing units under construction have taken a significant decline in 2024, reflecting broader challenges in the housing market. Building permits, a forward-looking indicator of housing conditions, have also declined, signaling potential future constraints within the housing market. With lower housing starts and fewer existing homes for sale, buyers may continue to find themselves with limited options and higher prices.

Despite these challenges construction spending in the United States has shown moderate growth over the past year. In September 2024, construction spending rose to a seasonally adjusted annual rate of $2,148.8 billion as the industry grew 4.6% over the past year ending in September.

Mortgage rates dropped to 6.08% in September, providing some much-needed temporary relief for homebuyers and raising the Housing Affordability Index to 105.5. The anticipation of lower rates continues to persuade homebuyers to hold off on their search until rates are lower, leading to limited activity in the housing market. The “locked in” effect, where homebuyers are likely to keep homes that were purchased when rates were low, is expected to naturally reduce over time.

Both mortgage rates and housing supply continue to play a crucial role in the housing market. Lower rates may improve housing affordability, providing support for consumers. The shift in rates will play a key role in the demand for housing. Supply for homes will need to rise to account for this shift in demand, or else we will likely see a rise in home prices. These opposing forces will lead to sustained balance within the housing market.

Business Cycle

Our internal labor market research indicates a weakening labor market this year, with steady declines in job openings, rising layoffs and discharges, and an increase in the average length of unemployment over the past six months. These trends suggest a late-cycle phase, accompanied by an uptick in red flags signaling a potential recession. Fortunately, we still have not seen a majority of our indicators turn red, which suggests the labor market is healthy enough to hold off any recession fears in the coming quarters.

Despite persistent challenges in the broader manufacturing sector, there are reasons for optimism as our manufacturing indicators show improvement. The positive momentum in our indicators highlights the gradual improvement since a dip in the late summer months. In fact, we have seen the trend across several sub-industries improve, from the late-cycle growth we saw in the previous quarters to healthier mid-cycle growth. This shift is encouraging and suggests a reduced risk of an economic downturn and suggests a healthy start to 2025.

Our consumer indicators show mixed signals and some uncertainty for the near future. A reduction in the personal saving rate as well as growth in services suggest strengthening in consumer spending. In contrast, several indicators highlight weaknesses, such as the decline in restaurant sales and slow growth in goods. These mixed signals within our research are in line with the uncertainty many consumers feel about the near future.

While heavily influenced by mortgage rates and supply/demand, our research also highlights supporting indicators that can signal where the housing market is in the business cycle. Indicators such as building permits and production of household appliances show weakness within the housing market and suggest a late-cycle phase. Despite some signs of weakness within the housing market, there are still many supporting indicators that show strength. Some early indicators, such as homes under construction and units authorized but not started, show support for the housing market. Furthermore, growth in home furniture retail sales and furniture employee hiring support our composite indicator which points to the mid-cycle phase for the housing market.

Equity

The U.S. markets enter 2025 with remarkable momentum, showing a clear “risk-on” response to President Trump’s ambitious growth agenda. This enthusiasm is evident across multiple asset classes, with rising equities, falling bond prices, a strengthening dollar, higher breakeven inflation rates, and surging cryptocurrency valuations. The market’s optimistic stance emerges against a complex backdrop of strong economic growth, elevated inflation, a cooling labor market, restrictive monetary policy, and rising fiscal deficits.

Trump Policy Impact

The incoming administration’s agenda centers on five transformative policies that could reshape the market landscape. The proposed tariff structure, reaching up to 20% broadly and 60% on Chinese goods, represents perhaps the most immediate challenge for markets. Companies face critical decisions about absorbing these costs or passing them on to consumers, with significant implications for both corporate margins and inflation. The commitment to deep spending cuts and significant deregulation creates potential opportunities across sectors, particularly in energy and financial services. Major tax cuts, including the extension of the 2017 Tax Cuts and Jobs Act, could significantly boost corporate earnings and consumer spending power. However, restrictive immigration policies threaten to tighten labor markets further, potentially accelerating wage inflation and affecting labor-intensive industries most severely.

The market response to these policies reveals both opportunities and challenges. On the positive side, corporate tax reductions and deregulation have historically driven market enthusiasm. Lower corporate tax rates could materially boost company profits and incentivize business investment, while reduced regulations across key sectors like energy, banking, and healthcare may decrease compliance costs and enhance profitability.

Historically, these business-friendly policies typically trigger positive market sentiment and could support continued market strength. However, significant risks accompany these potential benefits. The combination of tax cuts and increased spending could substantially expand the federal deficit, potentially leading to higher interest rates and heightened inflation concerns. The aggressive trade policies, particularly regarding China, risk disrupting established supply chains and increasing costs throughout the economy.

Tariffs typically create one-time price adjustments rather than persistent inflation. Currency dynamics help moderate impacts – a stronger dollar offsets import costs while supply chains show flexibility in avoiding tariff exposure through trade diversification. Market impact depends more on services inflation (61% of CPI) than imported goods inflation (18.5% of CPI). The washing machine tariffs of 2018-2023 demonstrate this pattern – after an initial price surge, costs normalized as manufacturers adjusted supply chains, with some foreign producers relocating production to the U.S.

Immigration restrictions could exacerbate existing labor shortages, driving up wage costs particularly in sectors heavily dependent on immigrant labor such as agriculture, construction, and services.

Success in navigating this environment requires distinguishing between negotiating rhetoric and actual policy implementation while monitoring company-specific abilities to adapt.

Despite these challenges, historical precedent suggests the current bull market’s momentum could persist if investors maintain their focus on business-friendly aspects of the agenda while discounting potential economic disruptions. Markets have demonstrated resilience through previous policy shifts when underlying economic fundamentals remain sound.

However, the actual market impact will largely depend on implementation specifics – which policies are prioritized, their timing, and how they interact with existing economic conditions. The market’s preference for policy certainty and gradual change rather than sudden disruption will play a crucial role in how these policies impact asset prices.

The broader economic environment, including Federal Reserve responses and global economic conditions, will significantly influence how markets digest these policy changes. This complex interplay between policy implementation and market dynamics requires investors to carefully balance potential opportunities against implementation risks as they position for 2025.

Federal Reserve and Trump Policy Interaction

The interaction between President Trump’s growth-oriented agenda and Federal Reserve policy creates an extraordinary set of challenges for 2025, with potential institutional conflict adding another layer of market risk. Multiple elements of Trump’s policy agenda carry inflationary implications that could force the Fed to maintain a more hawkish stance than the administration desires.

The proposed tariff structure would directly increase import costs across the economy. Immigration restrictions would likely tighten labor markets further, creating wage inflation pressures which could be amplified by planned tax cuts and fiscal stimulus measures. The Federal Reserve, operating under its mandate of price stability and maximum employment, could find itself in direct opposition to the White House’s growth agenda. Given the Fed chair’s statutory protection from presidential removal except “for cause,” any public conflict between President Trump and the Fed could create significant market uncertainty. Historical precedent suggests that markets react negatively to perceived threats to Fed independence, particularly when monetary and fiscal policies appear to be working at cross purposes.

Current market expectations for monetary easing conflict directly with the potential inflationary pressures from President Trump’s policies. Should the Fed determine that inflation risks require maintaining higher rates longer than the administration desires, public criticism from the White House could trigger market volatility. The situation becomes particularly delicate given the expanded federal deficits expected from tax cuts and spending initiatives. The Fed might face the challenging choice between maintaining price stability through higher rates or accommodating fiscal expansion through easier monetary policy. That, of course, risks reigniting inflation concerns.

The bond market appears particularly vulnerable to these policy crosscurrents. Growing federal deficits combined with inflationary pressures could require higher yields to attract investors, potentially creating stress throughout rate-sensitive sectors of the economy.

The timing and sequencing of policy implementation becomes even more critical in this context. Early implementation of tariffs before any Federal Reserve easing could trigger inflationary spikes and force the Fed to maintain higher rates longer than markets currently expect.

Tax cuts implemented without corresponding spending reforms could pressure the bond market, potentially driving yields higher across the curve and creating additional points of conflict between monetary and fiscal authorities. For investors, navigating these potential institutional conflicts adds another layer of complexity to an already challenging environment. Success in 2025 will require careful monitoring not just policy implementation and economic data, but also the evolving relationship between the Fed and White House.

Portfolio positioning may need to account for potential volatility spikes triggered by public disagreements over monetary policy, particularly if inflation proves more persistent than expected or economic growth falls short of administration targets. This complex dynamic between independent monetary policy and aggressive fiscal expansion creates a unique risk environment that could significantly impact market performance throughout 2025.

Economic Environment and Market Forces 2025

The U.S. economy demonstrates remarkable resilience entering 2025, exhibiting a powerful shift from late-cycle conditions back to mid-cycle characteristics. This economic repositioning creates an especially favorable backdrop for equity markets, as historical data shows mid-cycle periods typically generate average returns of 14% annually. The economy’s robust performance provides particularly strong support for cyclical sectors that tend to thrive during periods of economic expansion.

Significant tailwinds may support continued market strength in 2025. The anticipated Federal Reserve easing should create a positive environment for equity markets by reducing borrowing costs and making stocks relatively more attractive compared to fixed income investments. Companies carrying floating-rate debt will find particular relief as interest rates decline.

The U.S. maintains its position as a global economic leader, standing out against weaker growth in Europe and China, which enhances the attractiveness of U.S. equities to international investors. The resolution of election uncertainty has significantly boosted business confidence, with companies showing increased willingness to move forward with previously delayed investment plans.

Back-to-back years of 20%+ gains in 2023 and 2024 raise concerns about market exhaustion and limited potential for further multiple expansion. High concentration in mega-cap technology companies creates potential vulnerability for the broader market indices which are market – cap weighted.

Market volatility remains a key concern as uncertainty surrounds the specific implementation of President Trump’s policy agenda. Many businesses may delay significant investment decisions until they gain clarity on the policy landscape, potentially creating periods of economic weakness.

Market participants are likely to react strongly to both policy announcements and economic data releases, resulting in more pronounced price swings across asset classes.

The bond market could effectively cap equity market gains if Treasury yields remain elevated, and the Federal Reserve maintains its current policy stance. Current positioning data indicates heavy investment in equities, suggesting limited new buying power available to drive further market advances. Additionally, the implementation of significant tariffs poses substantial risks to companies’ global supply chains that have been optimized over decades, potentially affecting both corporate margins and inflation rates.

Despite these challenges, several factors may help support ongoing market strength. The yield curve’s steepening pattern historically correlates with improved performance across broader market segments, suggesting a supportive environment for market expansion beyond mega-cap stocks. Additionally, strong corporate earnings growth, projected at 12-15% for 2025, provides fundamental support for current market levels. The U.S. economy’s relative strength compared to other developed markets continues to attract global capital flows, providing another source of market support.

The interaction of these competing forces suggests a market environment in 2025 that may favor active management and careful sector selection over broad market exposure. While the economic backdrop remains supportive, elevated valuations and policy uncertainties require investors to be more selective in their positioning. Success will likely require balancing exposure to sectors benefiting from economic strength while maintaining sufficient quality focus to navigate potential volatility spikes.

Strong Earnings Expectations and High Valuations

The U.S. stock market enters 2025 demonstrating remarkable earnings strength while trading at historically elevated valuations. The S&P 500’s earnings performance has been particularly impressive. Corporate America has displayed notable resilience, with 75% of companies beating earnings estimates and delivering results 4.5% above expectations.

Revenue performance has been robust, growing 5.6% year-over-year for the sixteenth straight quarter. Companies have successfully maintained healthy profit margins of 12.2%, matching last year’s levels and exceeding the five-year average of 11.5%. This margin stability is particularly noteworthy given the challenging inflationary environment and ongoing supply chain pressures.

Looking ahead, analysts project even stronger growth, with fourth-quarter earnings expected to jump 12.0% and full-year 2025 earnings forecasted to surge 15.0%. However, these strong fundamentals are accompanied by increasingly stretched valuations. The S&P 500’s forward price-to-earnings ratio stands at 22.0, significantly above both its 5-year average of 19.6 and its 10-year average of 18.1. While high valuations alone do not necessarily predict a market downturn, they do suggest that future returns may be limited. A significant correction could occur if growth weakens, inflation spikes, or monetary policy stays tighter than markets expect.

The market exhibits notable sector divergences that highlight current investor preferences. The Technology sector appears particularly expensive with a forward P/E of 29.2, commanding premium valuations despite showing more modest growth prospects. In contrast, the Energy sector maintains the lowest P/E ratio at 14.9 despite showing the largest earnings decline (-24.8%).

This disparity underscores the market’s continued preference for growth over value stocks, even in the face of shifting economic conditions. The overall data suggests a strong fundamental earnings picture but increasingly stretched valuations compared to historical levels. While robust earnings growth provides support for higher stock prices, the elevated multiples could limit further upside unless earnings growth exceeds current expectations. This valuation challenge becomes particularly relevant given the market’s high expectations for 2025 earnings growth. The sustainability of these valuation levels will likely depend on several key factors:

- The ability of companies to meet or exceed aggressive earnings growth expectations

- The path of interest rates and their impact on equity risk premiums

- The successful implementation of growth-supportive policies without triggering significant inflation

- The maintenance of current profit margins in the face of potential wage and input cost pressures

This combination of strong earnings momentum and elevated valuations creates a complex environment for investors entering 2025. While the fundamental backdrop remains supportive, the high valuation starting point suggests the need for careful stock selection and increased attention to potential catalysts that could trigger multiple compression. Success in this environment may require focusing on companies with the strongest earnings visibility and ability to exceed current growth expectations.

The Case for Sector Rotation and Market Leadership

The market appears poised for a significant rotation beyond mega-cap technology dominance in 2025, though history suggests policy support alone doesn’t guarantee sector performance. During President Trump’s previous term, energy stocks became the worst-performing sector despite pro-fossil fuel policies, while under President Biden, the S&P 500 Global Clean Energy index fell 57.83% from his inauguration through November 29, 2024, despite his administration strong support for renewable energy. These examples underscore that sector performance depends on multiple factors beyond policy initiatives.

Financial institutions stand to benefit significantly from the steepening yield curve environment and proposed deregulation measures. Banks, particularly regional institutions, should see improved net interest margins as short and long-term rates spread widen. However, these benefits depend heavily on actual implementation of deregulation rather than mere proposals. Success will likely come to institutions with existing operational efficiency and strong risk management practices.

Energy companies face a complex landscape where individual company dynamics may matter more than broad sector exposure. While deregulation initiatives and increased infrastructure spending create opportunities, particularly in liquefied natural gas exports and domestic production, success will depend more on factors like asset quality and operational efficiency than policy support alone.

The industrial sector appears well-positioned to capitalize on reshoring initiatives driven by higher tariffs and domestic manufacturing incentives. Companies focusing on automation and productivity enhancement solutions should see increased demand as labor markets tighten due to immigration restrictions.

This trend particularly favors technology firms offering practical solutions to workforce challenges over traditional growth stories.

Consumer discretionary stocks require careful analysis beyond simple policy implications. Companies with strong domestic supply chains and demonstrated pricing power may prove more resilient than those heavily dependent on international sourcing. The ability to navigate potential tariff impacts while maintaining margins will be crucial.

Healthcare sector opportunities may concentrate in domestic manufacturing and supply chain security rather than broad sector exposure. Companies positioned for reshoring of critical medical supplies could see particular advantages, while traditional healthcare service providers face more mixed conditions.

On the losing side, import-dependent retailers face significant challenges from higher tariffs and supply chain disruptions. Labor-intensive industries could struggle with restricted immigration and rising wages, particularly in agriculture, construction, and services. Rate-sensitive sectors might face pressure if interest rates remain elevated, while highly leveraged small-caps could encounter financing difficulties.

Real estate faces mixed conditions where higher interest rates create near-term headwinds, but infrastructure spending and economic growth provide longer-term opportunities. Industrial and data center real estate investment trusts should benefit from reshoring initiatives and continued digital transformation. Success in this rotation environment requires looking beyond headline policy initiatives to understand specific company positioning, balance sheet strength, and ability to navigate both policy implementation and broader economic conditions.

The historical disconnect between policy support and sector performance suggests maintaining diversification while focusing on company-specific factors that support sustainable growth regardless of policy outcomes.

International Markets Dynamic

European markets face mixed prospects as they navigate U.S. trade policy changes. Countries with strong domestic manufacturing bases like Germany could benefit from trade diversions away from China, though export-dependent economies face headwinds from global trade restrictions.

European financials appear particularly attractive given lower valuations compared to U.S. peers and the European Central Bank’s likely pause in tightening.

In the Asia Pacific region, Japan presents compelling opportunities as corporate governance reforms continue and companies maintain high cash balances. The weak yen supports exporters, while domestic-focused small cap companies benefit from restructuring.

Indian markets present strong domestic growth potential, with a degree of insulation from U.S.-China trade tensions.

Southeast Asian nations may benefit from supply chain diversification, though commodity-exporting nations face pressure from potential global growth slowdown.

Fixed Income

While some might not realize it, 2024 was marked by periods of notable strength across various fixed income sectors, underpinned by robust fundamental drivers. The U.S. Aggregate Index delivered its second-highest quarterly return, 5.2%, since 1996 in Q3 2024, fueled by rising expectations of an aggressive rate-cutting cycle by the Federal Reserve. All the while corporate issuance reached record highs as issuers capitalized on favorable funding conditions.

Despite this impressive performance, the market witnessed some challenges towards the end of the year, with Treasury yields rising since mid-September. Looking ahead, the key question is whether the supportive backdrop of Fed Rate cuts that aided fixed income returns in 2024 will persist, or if new dynamics will emerge to reshape the investment landscape.

Economic Backdrop

The U.S. economy is expected to demonstrate ongoing resilience in 2025, even as growth moderates from the robust levels seen in previous years. Gross Domestic Product (GDP) expansion is projected to stabilize in the 2.0-2.5% range, slightly down from its most recent reading of 2.8%, underpinned by healthy consumer spending and a gradual recovery in business investment. Inflation has made progress toward the Federal Reserve’s 2% target but remains somewhat elevated. Excluding the volatile food and energy categories, core PCE rose 2.7% in the 3rd quarter of this year.

This macroeconomic backdrop provides a broadly supportive foundation for fixed income markets, but also presents some challenges. On the one hand, the combination of steady growth and contained inflation reinforces the case for a stable monetary policy stance, which could help anchor short-term yields. On the other hand, any upside surprises to growth or inflation could prompt a reassessment of the policy outlook, potentially leading to bouts of volatility.

Federal Reserve Policy

The Federal Reserve is set to play a pivotal role in shaping bond market dynamics in 2025. With inflation approaching target levels and growth stabilizing, the Federal Reserve is expected to maintain a data-dependent approach to policy adjustments. Chairman Powell has indicated the central bank’s intention to reduce what he calls “policy strain” through a measured easing cycle.

Recent policy actions have included a 25-basis-point reduction in November 2024, following a 50-basis-point cut in September 2024. The Federal Open Market Committee’s latest projections suggest four additional 25-basis-point reductions through 2025, though the path remains dependent on incoming economic data.

However, the potential for policy surprises cannot be ruled out, particularly if incoming data challenges the Fed’s assessment of the growth and inflation outlook. A stronger-than-anticipated economic recovery or a more pronounced pickup in inflationary pressures could diminish expectations of future rate cuts, leading to a repricing of short-term yields and further, a steepening of the yield curve.

On the other hand, if economic growth falters or job numbers come in weaker than expected, the Federal Reserve may need to explore further monetary easing, which could involve revisiting non-traditional policy instruments. This scenario could lead to a rally in longer-dated bonds and a further flattening of the yield curve.

The key takeaway is that monetary policy uncertainty is likely to remain a significant driver of bond market volatility in 2025. Investors will need to stay attuned to shifts in the Fed’s rhetoric and be prepared to adjust their portfolios accordingly.

Duration Strategy

In an environment characterized by monetary policy uncertainty and the potential for yield curve shifts, active duration management will be crucial.

Market conditions will likely create tactical opportunities for duration adjustments throughout the year. When the yield curve steepens, particularly in response to stronger growth or inflation data, investors may find attractive entry points to extend duration. During periods of curve flattening or inversion, a more defensive positioning focused on shorter-dated maturities may be prudent. Successful implementation of these tactical shifts requires careful analysis of market technicals, fundamental drivers, and investor sentiment patterns. As Warren Buffett’s timeless advice suggests, investors should “be fearful when others are greedy and greedy when others are fearful” – a principle particularly relevant to duration management when markets exhibit extreme positioning. These moments of market dislocation often present the most compelling opportunities for tactical asset allocation adjustments.

The yield curve’s various segments respond differently to market forces, creating opportunities for strategic positioning. Front-end yields typically align closely with Federal Reserve policy expectations, providing a more predictable return profile. Meanwhile, intermediate and longer-dated maturities demonstrate greater sensitivity to shifts in economic growth, inflation expectations, and broader market sentiment. A thoughtful allocation across these curve segments allows investors to diversify their sources of return while maintaining flexibility to adjust positioning as market conditions evolve. This segmented approach to curve positioning enables portfolio managers to express specific views on monetary policy, economic fundamentals, and relative value opportunities while maintaining a balanced risk profile.

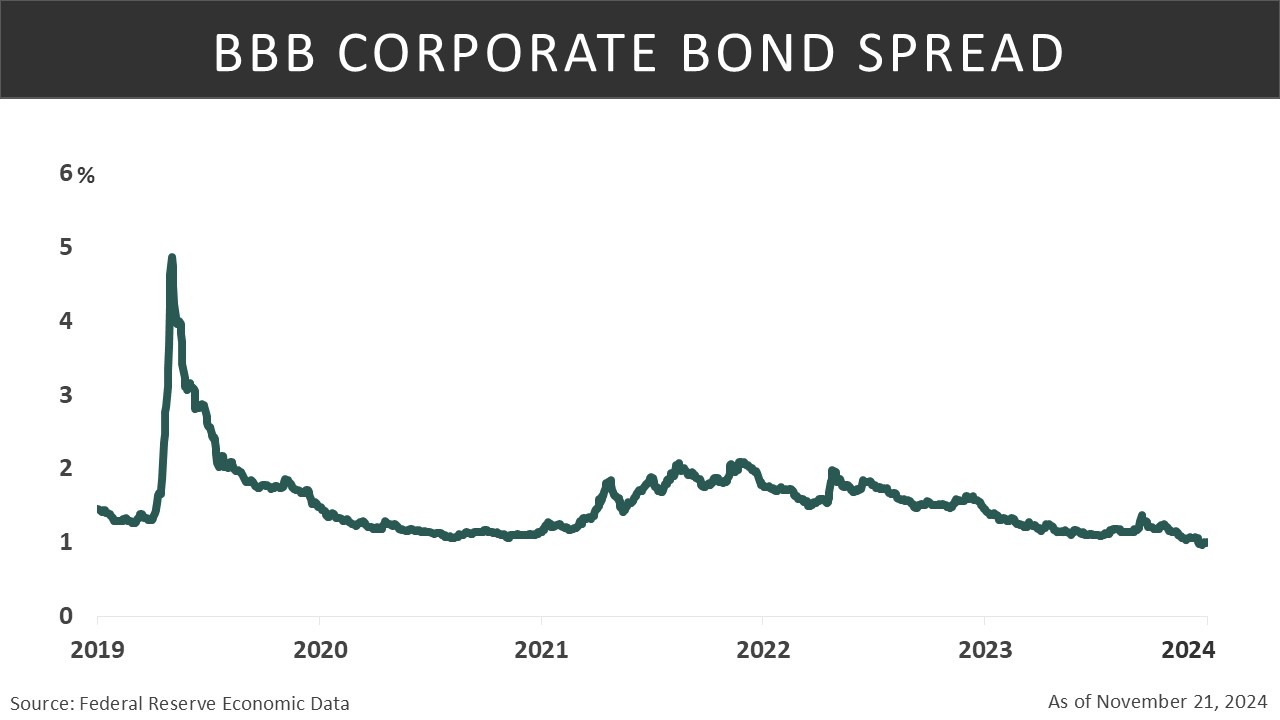

Credit Spreads

Credit spreads, which measure the yield differential between Treasury and non-Treasury securities, are expected to trade in a narrow range throughout 2025. Three key factors support this compressed spread environment: persistent investor demand for yield-generating assets, robust corporate balance sheets and earnings, and the Federal Reserve’s accommodative policy stance. Nevertheless, valuations across fixed income sectors appear stretched by historical standards. This is particularly evident in higher-quality segments, where spreads have already tightened significantly, leaving minimal potential for additional compression. The combination of tight spreads and full valuations suggests returns in 2025 will likely be driven more by income generation than by further spread tightening.

Investment-grade corporate bonds are positioned to maintain relatively stable spread levels in 2025, though market dynamics warrant careful attention. While strong underlying credit fundamentals provide support, any deterioration in economic conditions or broader market sentiment could trigger spread widening, particularly in lower-rated segments of the market. In this environment, successful portfolio management demands intensive issuer-level analysis focusing on companies that demonstrate financial discipline through multiple market cycles. Companies with strong market positions, predictable cash flow generation, and conservative balance sheet management merit particular attention. Sector positioning will also play a crucial role in performance outcomes. Defensive sectors, particularly utilities and consumer staples, offer more attractive risk-adjusted opportunities given their earnings stability and essential service nature. In contrast, cyclical sectors face greater uncertainty as questions about economic growth persist, suggesting a more selective approach to these segments is warranted. We would also look to favor those sectors where regulations may be relaxed by the incoming administration.

High-yield bonds may offer relatively more attractive spread opportunities, especially among higher-quality issuers with improving credit metrics. However, a selective approach is warranted, as default rates are expected to rise modestly from current low levels. In-depth credit analysis and a focus on companies with strong liquidity profiles will be key to navigating this segment effectively.

Municipal bonds may deliver additional gains in 2025, as they have lagged the rally witnessed in other taxable sectors. The municipal yield curve has been normalizing from its previous “U” shape, reflecting a shift in rate cut expectations and an uptick in demand for longer-dated bonds. This trend could persist if the Fed remains on its easing path. Spreads on the short end of the municipal curve appear particularly attractive, benefiting from ongoing outflows from short-term funds and robust demand for tax-exempt income.

Potential Surprises

While the base case for 2025 is constructive, several risks could alter the trajectory of the bond market. The unwinding of central bank balance sheets, known as quantitative tightening (QT), is expected to exert upward pressure on longer-dated yields. Combined with trade policy risks, geopolitical tensions, and the potential for inflation surprises, this could contribute to periods of heightened volatility.

Political uncertainties, both domestically and abroad, also have the potential to unsettle markets. The implementation of President Trump’s proposed policies on trade, immigration, deregulation, and fiscal stimulus could have wide-ranging implications for growth, inflation, and interest rates. Navigating these policy crosscurrents will require a deft hand and a keen eye for potential market dislocations. Geopolitical flare-ups and the ever-present threat of unexpected shocks also warrant a cautious approach to risk management. While tensions in the Ukraine-Russia war are already heightened, any further escalation may cause a flight to quality in the bond market. The same can be said for potential issues that continue in the Middle East between Israel and Hamas.

While not of the same magnitude, a different type of war may occur depending on tariffs, a trade war, specifically with China. Should this economic battlefront grow more heated than anticipated, the Chinese may sell U.S. Treasury notes and bonds at high speeds, pushing down prices and elevating bond yields.

Conclusion

The 2025 U.S. market outlook is complex, shaped by the powerful interaction of economic resilience, strong corporate earnings, elevated valuations, transformative President Trump administration policies, and uncertainty surrounding the Federal Reserve’s monetary stance.

Looking at key economic indicators, the labor market shows some weakening trends, with declining job openings, rising layoffs, and longer unemployment durations signaling late-cycle risks. However, most indicators suggest the labor market remains resilient. Manufacturing is improving, with sub-industries shifting from late-cycle to healthier mid-cycle growth. The housing market presents a mixed picture, with late-cycle traits in building permits and appliance production balanced by mid-cycle strengths in construction and furniture sales. Consumer spending is strong in services but weaker in goods and restaurants, reflecting broader uncertainty.

President Trump’s ambitious agenda, which includes tariffs, deregulation, spending cuts, tax reductions, and restrictive immigration policies, presents both significant opportunities and risks for investors. The U.S. economy’s shift back to mid-cycle characteristics provides a favorable backdrop, particularly for cyclical sectors. Corporate earnings momentum remains impressive, with robust revenue growth and stable margins supporting higher equity prices. However, historically high stock valuations suggest future gains may be more limited without earnings growth exceeding expectations.

In this multifaceted landscape, investment success will favor a balanced approach that combines targeted exposure to sectors and companies positioned to benefit from policy tailwinds with prudent risk management. Financials, industrials, energy, and select healthcare and technology companies appear attractively situated. However, investors should avoid indiscriminate sector bets and instead focus on company-specific analysis, emphasizing firms with strong fundamentals, pricing power, domestic supply chains, and the ability to navigate policy-related challenges.

Internationally, markets offer selective opportunities, with Europe and Japan presenting compelling prospects. Emerging markets, while attractive over the long term, may face near-term volatility. Across all geographies, a focus on quality, value, and effective policy response is prudent.

The fixed income market presents a nuanced outlook, offering both challenges and opportunities. The economic backdrop remains broadly supportive, with steady growth and well-anchored inflation. However, the potential for monetary policy surprises and periodic bouts of volatility cannot be ignored. In this environment, a dynamic approach to duration management and a selective approach to credit risk will be essential. Investors should actively adjust portfolio positioning as conditions evolve, maintain a focus on quality, and ensure ample liquidity to effectively navigate the road ahead. While the temptation to reach for yield may be strong, discipline and prudence should remain the guiding principles.

Ultimately, while the 2025 market path is likely to be complex, it is also full of potential for astute investors able to navigate the dynamic interplay of economic trends, earnings strength, policy transformations, and valuation constraints. By coupling judicious positioning with vigilant risk oversight, investors can try to seize the opportunities of this consequential market moment while skillfully managing its challenges. The road ahead may be winding, but with insight and agility, it has potential to lead to a prosperous investment horizon.

For Investors:

Equities

- Focus on sectors benefiting from President Trump’s policies: Financials (deregulation), Utilities (powering AI data centers), and Industrials (reshoring)

- Target companies with strong domestic supply chains and proven pricing power

- Exercise caution with import-dependent retailers and labor-intensive industries

- Maintain selective exposure to technology, emphasizing practical solutions such as software

- Consider mid and small cap stocks as Fed easing provides support through lower borrowing costs

Fixed Income

- Implement active duration management to help capitalize on yield curve shifts

- Explore opportunities in municipal bonds, particularly in short-duration securities

- Maintain defensive positioning in Utilities and Consumer Staples sectors

- Consider higher-quality high-yield issuers, including convertible bonds, with strong liquidity profiles

What Can Go Wrong

- Policy implementation risks, particularly regarding tariffs and trade relations

- Federal Reserve-White House conflicts over monetary policy

- Persistent inflation preventing expected rate cuts

- Further geopolitical escalation in Ukraine or Middle East

- Chinese reaction to trade policies, including potential Treasury sales

- Labor market deterioration beyond current expectations

Disclosure

This information is of a general nature and does not constitute financial advice. It does not take into account your individual financial situation, objectives or needs, and should not be relied upon as a substitute for financial or other professional advice to assess, among other things, whether any such information is appropriate for you and/or applicable to your particular circumstances. In addition, this does not constitute an offer to sell, or the solicitation of an offer to buy, any financial product, service or program. The information contained herein is based on public information we believe to be reliable, but its accuracy is not guaranteed.

Investing involves risks, including loss of principal. Past performance is no guarantee of future results.

Definitions

*Consumer Price Index (CPI): An index of the variation in prices paid by typical consumers for retail goods and other items.

*The Purchasing Managers’ Index (PMI) is an indicator of the prevailing direction of economic trends in the manufacturing and service sectors. The indicator is compiled and released monthly by the Institute for Supply Management (ISM), a nonprofit supply management organization.

*Price/Earnings Ratio: ratio for valuing a company that measures its current share price relative to its earnings per share (EPS).

*Growth: A company stock that tends to increase in capital value rather than yield high income.

*Value: A value stock is a security trading at a lower price than what the company’s performance may otherwise indicate.

*Quantitative Tightening: monetary policies that contract, or reduce, the Federal Reserve System (Fed) balance sheet.

*Basis Point: one hundredth of one percent, used chiefly in expressing differences of interest rates.

*BBB Bonds: An investment grade is a rating that signifies a municipal or corporate bond presents a relatively low risk of default. “BBB” (medium credit quality) are considered investment grade.

*Yield Curve: A yield curve is an economic indicator that tracks the relationship between long- and short-term bond yields.

*U.S. Aggregate Bond Index: Designed to measure the performance of publicly issued US dollar denominated investment-grade debt.

*S&P 500 Index: S&P (Standard & Poor’s) 500 Index: is a market-capitalization-weighted index of the 500 largest US publicly traded companies.

*NASDAQ: is a global electronic marketplace for buying and selling securities.

*Russell 2000 Index: a stock market index that measures the performance of the 2,000 smaller companies included in the Russell 3000 Index.

*Indexes are not managed. One cannot invest directly in an index.