This is the first article in a series about the TSP, or the Thrift Savings Plan. Essentially it is a retirement plan for groups of people who work for the federal government. Mail carriers, military personnel, and civil government workers are the main groups of people who make up the participants in the plan. If you’re reading this, you are probably a part of one of the groups. We hope this helps you understand how the TSP works.

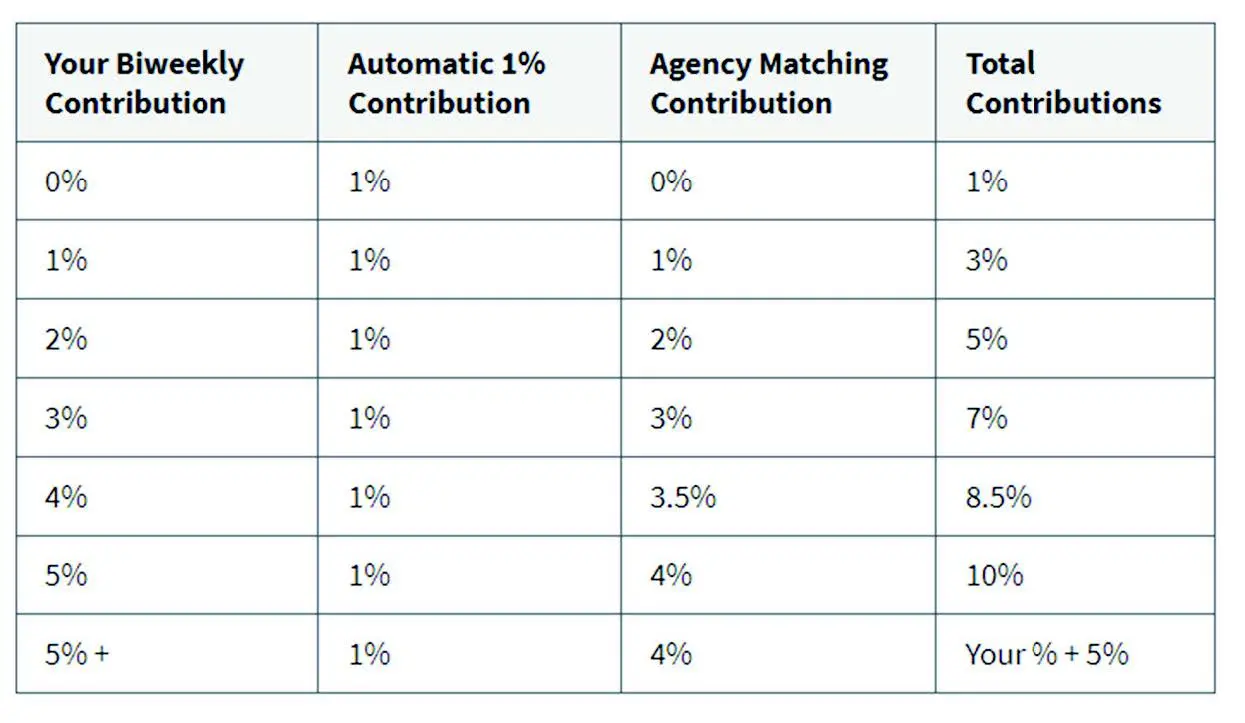

Like other employer retirement plans, the federal government makes contributions to your TSP account. No matter whether you contribute or not, the federal government contributes the equivalent of 1% of your pay each pay period. The government also contributes the equivalent of 100% of the first 3% that you contribute. If you contribute between 4-5% they provide a 50% match for the 4th and 5th percent. So, in total, if you contribute 5% of your pay to your TSP account, you will receive a 1% automatic contribution, a match on the first 3% and then a half percent for the 4th and 5th percent for a total extra contribution of 5%, made by the federal government. With the total match and your own contribution, a 5% employee contribution will be added to the 5% government contribution for a total of 10%.

Something unique about the TSP plan is that its vesting schedule is more generous than other employers. Typically, an employee must work at a company for 3-5 years before they are entitled to keep the match their employer contributes. The match the government contributes is vested immediately, meaning even if you leave government employment quickly you still get to keep the match. The 1% automatic contribution, on the other hand, has a vesting schedule. It is somewhat dependent on your role in the government, but if you work for the government for 2-3 years you get to keep the 1% agency contribution and match. The money you contribute to the TSP is always yours no matter how long you work for the government. After all, it is your money.

Contribution Limits

How much can you contribute to the TSP? In 2023 an employee can contribute up to $22,500 per year. Most of America has not adequately saved for retirement so the IRS has added a catch-up provision for those 50 and older. They can contribute an additional $7,500 for a total of $30,000 per year.

If you started with the government after October 1, 2020 you are automatically enrolled at 5% of your salary. To determine your contribution amount either consult your Leave and Earnings Statement (LES) or log on to your agency or service’s electronic payroll system. You can also start, change, or stop your TSP contributions through the payroll system. You will need to know the percentage or amount you would like to contribute per pay. If you want to contribute the maximum before the end of the calendar year, you will need to divide the contributions still needed by the remaining pay periods and that will give you the dollar amount to put in the payroll system. Keep in mind that the maximum amount you can contribute depends on age. Don’t forget to add that extra catch-up provision if you are 50 or older.

You’ll need one other piece of information to finish your contribution election in the payroll system. Where do you want to contribute the money?

Different Types of Accounts

The TSP has two different types of accounts for non-deployed employees, Traditional (pretax) and Roth (after tax). The Roth account is a relatively new option. If you select a Roth account for your contributions, you will pay taxes when the money is contributed. The advantage to the Roth account is if you follow the IRS’ rules you won’t have to pay tax when a withdraw is taken. This can be very beneficial because any growth in the account is tax free. If you think your taxes will be higher in your retirement years versus now, a Roth account may be a good option for you. Even if all your personal TSP contributions are made to your Roth account, you will also have a Traditional account because the agency contribution and match previously discussed are put in a Traditional account, not the Roth account. This results in having Roth and Traditional account balances.

If you select your contributions to go to the Traditional account, you receive a tax break today. Any contributions made to this account reduce your taxable income for that year. Contributions are taken from your paycheck before tax is withheld. This provides tax savings now. When the money is withdrawn from the TSP you will have to pay income tax. People contribute to the Traditional account when they think their tax bracket will be higher now rather than in retirement. Both the Traditional and the Roth accounts have the benefit of growing tax deferred. You don’t pay tax as it grows.

If you are scratching your head wondering which account to select, we can help at James. We analyze your situation to help determine what type of account is the best option for you. Tax brackets now and in retirement aren’t the only considerations. Be sure to check out the other two articles in the series. We will explain the investment options inside the TSP and detail ways you can withdraw from the TSP.

– The James Team