June 2023

Key Insights

- The “Debt Ceiling” debate in May had a negative impact on financial markets.

- The banking crisis continues to have a lasting effect as banks tighten credit standards.

- The Federal Reserve is divided about the future interest rate path due to persistent inflation and a resilient job market.

- The recent market rise has been driven primarily by a small group of mega-cap stocks.

- The timing, severity, and duration of the highly anticipated recession are currently subjects of extensive discussion and speculation.

Monthly Recap

The financial headlines in May were largely focused on the political deadlock over the U.S. “debt ceiling.” It is anticipated that, similar to previous instances, a lastminute agreement will be reached before the government exhausts its funds to meet its obligations. Treasury Secretary Janet Yellen has warned that the U.S. could potentially start missing debt payments by June 5th.

On May 24th, yields on short-dated Treasuries continued to climb as investors sought higher compensation due to the risk of default. Securities maturing on June 1st saw their yield surpass 7%, while those maturing on May 30th had yields of around 3%. It is important to recognize that the U.S. Treasuries market, valued at approximately $24 trillion, is the largest and most liquid bond market globally, serving as the bedrock of the global capital structure.

Furthermore, the credit default swap (CDS) cost for insuring against the non-payment of U.S. government debt is currently higher than that of several emerging markets, which have previously experienced defaults and possess lower credit ratings compared to the United States. Any temporary default could have catastrophic consequences.

The other significant headline was the enduring impact of the banking crisis. In early March, the financial markets faced notable resemblances to the 2007-08 financial crisis as the U.S. government utilized the systemic exception to guarantee the deposits of two major regional banks, namely Silicon Valley Bank and Signature Bank. Furthermore, in early May, JP Morgan Chase Bank assumed control of First Republic Bank. The concern over the potential spread of bank runs and doubts regarding the Federal Reserve’s (Fed) ability to achieve both financial stability and price stability unsettled the financial markets.

The regulatory response to the recent banking challenges has indeed been swift and significant, with the Federal Reserve taking steps to provide favorable capital access to the banking sector. These measures indicate the current turbulence is unlikely to pose a systemic risk. However, there are valid concerns surrounding an economic slowdown, increased funding costs, continued outflows of deposits to money market funds, and forthcoming stricter regulations.

As a result, banks are compelled to implement stricter credit policies. The most recent Senior Loan Officer survey conducted by the Federal Reserve confirms a further tightening of credit standards, intensifying the impact of the Federal Reserve’s interest rate hikes. Consequently, the borrowing capacity of both businesses and individuals is reduced.

The banking issues mentioned have had a noticeable impact on the performance of regional bank stocks. This is evident in the performance of the S&P Regional Bank Select Industry index, which experienced a decline of 8.8% in May and a year-to-date loss of 33.2%.

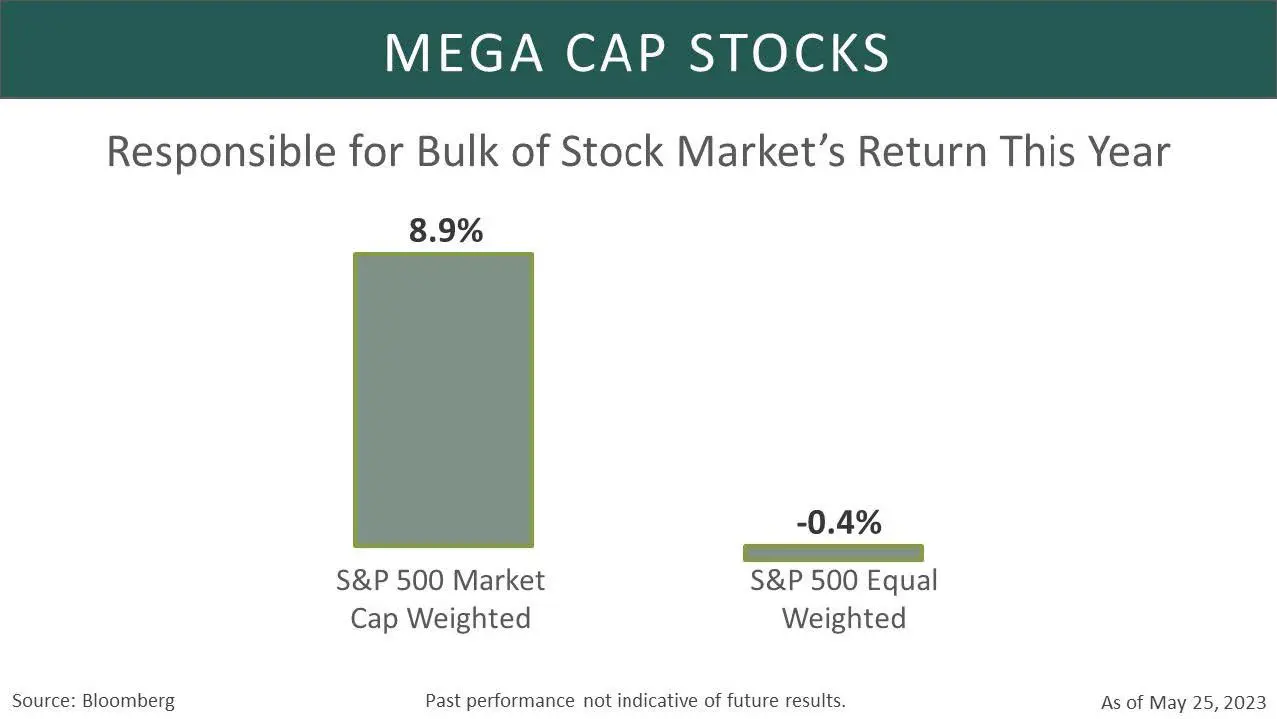

Other market segments have demonstrated stronger performance, particularly capitalization-weighted indexes where mega-cap companies with robust balance sheets, ample cash reserves, and diversified global revenue streams have outperformed.

The S&P 500 cap-weighted index has experienced a yearto-date increase of 9.6%, while its equal weight counterpart has incurred a 0.7% loss during the same period. The notable dominance of prominent companies like Apple, Nvidia, and the FANG stocks (Facebook, Amazon, Netflix, Google), which collectively constitute 50% of the Nasdaq 100 index, has propelled the index to a 7.7% gain in May and an impressive year-to-date increase of 30.8%.

The significant increase in the value of these predominantly mega-cap tech companies can also be attributed to the expectation that the Federal Reserve may halt its streak of eleven consecutive interest rate hikes, with the possibility of rate cuts on the horizon. Growth-oriented companies, particularly those with long-term projected cash flows, stand to benefit from a lower discount rate, leading to an enhancement in their valuation.

Minutes from the Fed May 2nd-3rd meeting revealed that policymakers expressed uncertainty regarding the extent of necessary policy tightening. They considered factors such as the slower-than-expected progress on inflation and the resilient labor market, while also weighing the potential risk of a credit crunch following the recent banking turmoil.

This exceptional performance of tech companies is reflected in the outperformance of growth stocks compared to value stocks by a substantial margin in May. Additionally, most sectors experienced declines during this period, except for the technology, communication services, and consumer discretionary sectors, which showcased notable resilience and positive performance.

Bonds of all maturities experienced a sell-off in May, resulting in higher yields as uncertainty surrounding the “debt ceiling” and the banking crisis persisted. When yields rise, bond prices typically decline. The two-year U.S. Treasury yield, which is particularly responsive to Federal Reserve policy, increased from 4.00% at the end of April to 4.41%. The U.S. Aggregate Bond Index (Agg) recorded a loss of 1.1% in May.

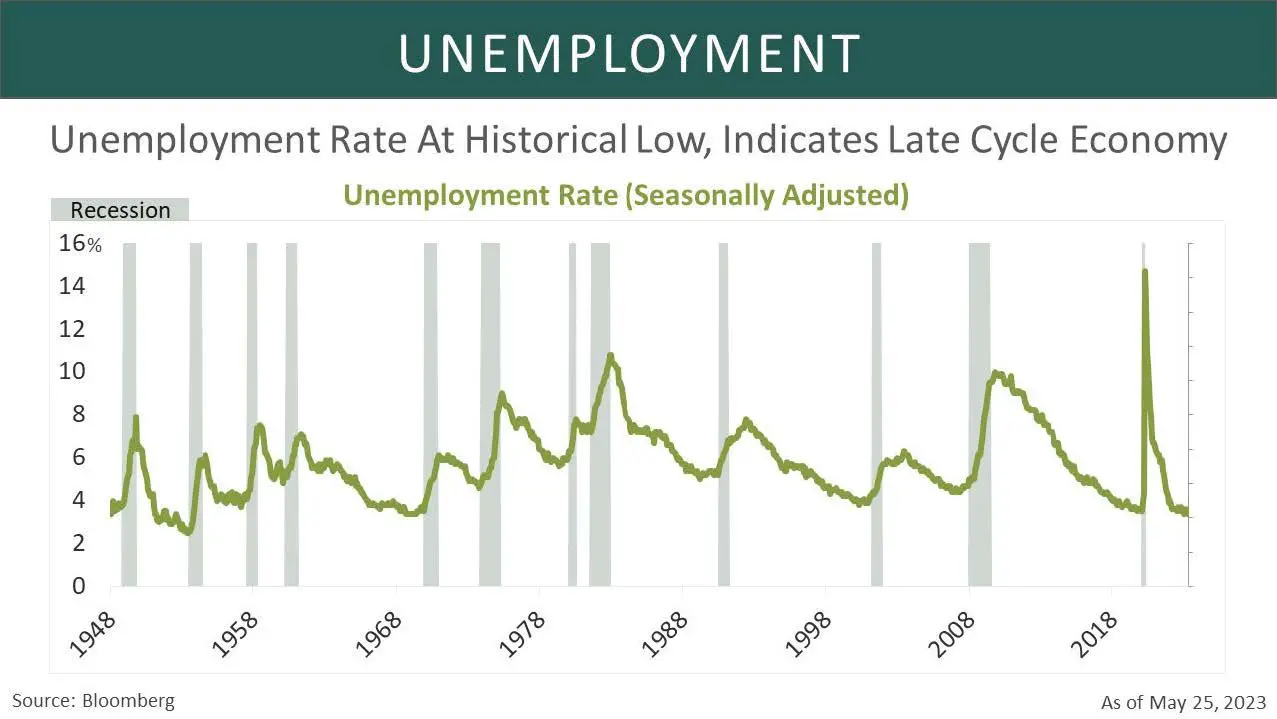

On the economic front, the news was upbeat in May. In April, there was a notable increase in hiring, resulting in a decline in the unemployment rate to 3.4%. Moreover, there has been a rise in labor force participation. Auto sales experienced a surge, reaching the highest level in nearly two years. Retail sales, in general, saw improvements, and there was an uptick in factory production.

U.S. companies reported earnings that exceeded expectations during the first quarter. However, companies in the real estate and financial sectors faced difficulties due to banking-related stress and concerns within the commercial estate market.

Despite this better-than-expected economic backdrop, a majority of economists surveyed by Bloomberg foresee a potential recession in the future. However, there is uncertainty regarding the severity of the recession, whether it would be a hard landing or a soft landing, as well as the timing of its occurrence, whether it would happen later this year or early next year.

Hard Landing vs. Soft Landing

Hard Landing

A hard landing refers to a swift and severe economic downturn characterized by a substantial decline in equity markets, high levels of unemployment, decreasing consumer spending, and an overall contraction in economic activity. This situation can have detrimental effects on businesses, households, and the overall economy. Monitoring various indicators can provide valuable insights to determine if a hard landing is imminent.

One of the primary indicators of an economic downturn is an increase in the unemployment rate. When the economy is weak, companies face financial challenges as growth slows down, leading to workforce reductions. Consequently, there is a surge in job losses, making it challenging for individuals to find new employment opportunities. Additionally, monitoring initial jobless claims can serve as a valuable leading indicator for the labor market. An upward trend in initial jobless claims suggests potential weakness in the labor market and signals a possible future rise in the unemployment rate.

Furthermore, a decline in consumer spending can indicate the potential onset of a hard landing. During periods of financial uncertainty, individuals tend to reduce their spending on non-essential items, resulting in a decline in the consumption of goods and services. Monitoring retail sales figures for luxury goods and leisure activities can offer valuable insights into consumer behavior and the overall economic well-being. A rapid decline in these segments could potentially serve as an early warning sign of forthcoming challenges and suggest the possibility of economic trouble ahead.

Another significant area of the market that can serve as a signal of economic trouble is the manufacturing sector. A decline in this segment often indicates weakness in overall economic growth. Reduced industrial output, weak factory orders, and declining exports all point to a slowdown in production and a decrease in overall demand.

Additionally, a sudden and substantial decline in the stock market can be a telling sign of an economic contraction. Sharp drops in major stock indices, accompanied by heightened volatility and panic selling, indicate increasing pessimism among investors and a decline in confidence in the economy. This, in turn, can further contribute to market declines.

In summary, a hard landing for the economy is typically characterized by a combination of indicators, including rising unemployment rates, declining consumer spending, contracting manufacturing sector, and stock market declines. Monitoring these factors can provide valuable early warnings of an impending economic recession.

Fortunately, at present, we do not observe all of these indicators signaling imminent trouble. The economy continues to demonstrate strength with notable wage growth, robust consumer spending, and strong job growth. The unemployment rate is near historically low levels, comparable to those last seen in the 1950s. Although initial jobless claims have shown an upward trend, job openings remain high, and it appears that workers are not encountering significant difficulties in finding new employment opportunities. Moreover, economic growth remained positive in the first quarter, with gross domestic product (GDP) expanding by 1.3%. Estimates for secondquarter growth also remain robust.

However, certain issues are emerging within the markets that raise concerns. Inflationary pressures are easing, yet they continue to erode consumer savings, leading individuals to accumulate more debt to cope with rising prices. Such a trend is not sustainable in the long run and can adversely impact both consumers and the overall economy.

Moreover, recent developments in the banking industry, such as the collapse of Silicon Valley Bank and First Republic, have rattled the sector. Consequently, lending standards have tightened as a result of these banking failures. The financial sector is often considered an indicator of the overall health of the economy. Presently, the impact seems contained, but if contagion were to occur, it could signal trouble on a broader scale.

Soft Landing

There is no official definition for soft landing of the economy. However, most economists agree that the Federal Reserve achieves a soft landing through its monetary policies when inflation returns to the target level of around 2% without a significant increase in unemployment. In terms of headline inflation, there has been a gradual decline from its peak of 9.1% in June 2022, and as of the end of April 2023, it stands at 4.9%. Core inflation, which excludes volatile food and energy prices and is of particular concern to the Fed, has remained stubbornly around 5.5% year-over-year for the past four months. It is 1% lower than its peak in October 2022, but still double the Fed’s target. On the other hand, unemployment is currently at a historically low level of 3.4%. Some economists argue that a core inflation rate below 3% and an unemployment rate between 4% and 5% would roughly align with a soft-landing scenario.

The economy is currently not in a recession. Retail sales numbers for April indicate strong consumer spending. The consumer is supported by robust monthly job creation and excess savings. This is also confirmed by state coincident indexes that are based on employment and income data. State coincident indexes, which are based on employment and income data and monitored by the Philadelphia Fed at the state level, continue to show widespread growth across the nation. These state-level conditions affirm that the economy is not currently in a recessionary phase.

Furthermore, the Atlanta Fed’s Nowcasting Model, which incorporates input data into a forecast as it becomes available, suggests that GDP growth is on track for 2.9% in the second quarter as of May 17th, which represents the mid-point of the quarter.

The soft-landing narrative is supported by several arguments. First, consumer spending, which accounts for two-thirds of the U.S. economy, has been strong. Consumers have shown a particular appetite for spending on services, driven by a desire for experiences after enduring the pandemic for two years. Airlines and cruise lines are reporting record bookings for the upcoming summer season, indicating robust demand for services. Although spending on goods is relatively weak, the strength in services spending more than compensates for this weakness.

The consumer’s ability to sustain spending is underpinned by three key factors. First, there are excess savings accumulated during the pandemic period, providing a cushion for continued expenditure. Second, income from the resilient labor market supports consumer purchasing power. Lastly, the wealth effect, influenced by factors such as rising home prices and stock market gains, further boosts consumer confidence and spending.

Overall, these factors contribute to the narrative of a soft landing, as the consumer continues to drive economic activity through robust spending supported by savings, income, and wealth effects.

According to Bloomberg Economics, cumulative excess savings across all income levels are projected to reach $1.35 trillion. Saving behavior is influenced by demographics and wealth accumulation, resulting in wealthier households holding a majority of these savings with a lower propensity to consume. However, households in the bottom 60% of the income distribution are estimated to have less than two months’ worth of spending power in the form of excess cash balances.

Despite economic challenges, the labor market remains resilient. Wage growth continues to be robust, and inflation is easing, supporting real income compared to previous months. Additionally, consumers still have the ability to borrow, as their credit card balances as a percentage of disposable income are slightly below pre-pandemic levels.

Moreover, lower mortgage rates in 2020 and 2021 allowed many households to refinance their mortgages, resulting in average monthly savings of $220, according to recent research from the Federal Reserve Bank of New York. Housing prices remain elevated and are experiencing single-digit growth, indicating that homeowners still possess healthy equity that can be utilized if needed.

In summary, these various factors may contribute to keeping the economy stable until inflationary pressures have subsided. This could result in a soft landing, characterized by sluggish but positive economic growth, a more relaxed labor market, and controlled inflation. This scenario would allow the Federal Reserve to consider easing monetary policy again, thereby stimulating economic growth further.

Conclusion

May’s financial headlines were dominated by the political deadlock over the U.S. “debt ceiling” and the lingering impact of the banking crisis. While a resolution to the debt ceiling issue is expected, the potential consequences of a temporary default on U.S. debt remain a concern.

The enduring effects of the banking crisis have prompted banks to adopt stricter credit standards. Moreover, the interest rate hikes implemented by the Federal Reserve, combined with the tightening of credit standards, are placing additional constraints on the borrowing capacity of both businesses and individuals.

The stock market performance has been mixed, with capitalization-weighted indexes outperforming. Mega-cap tech companies have been driving market gains, fueled by expectations of a pause in interest rate hikes. The minutes from the Federal Reserve meeting highlighted policymakers’ uncertainty regarding necessary policy tightening, considering factors such as inflation progress and the labor market.

In the bond market, yields rose due to the persistent uncertainty surrounding the “debt ceiling” and the banking crisis, resulting in a sell-off of bonds. May brought positive economic news, including increased hiring, declining unemployment, and improvements in auto sales and retail sales. However, concerns persist regarding the possibility of a future recession, although the severity and timing of such a downturn are uncertain.

Given these developments, it is advisable to approach the current situation with caution. Investors should focus on large companies with strong revenues, defensive sectors, and high-quality bonds. The trajectory of the economy and financial markets will continue to be influenced by factors such as the resolution of the debt ceiling issue, the response to the banking crisis, and the Federal Reserve’s monetary policies.

Sincerely,

The James Research Team

This material is distributed by James Investment Research, Inc. and is for information purposes only. No part of this document may be reproduced in any manner without the written permission of James Investment. It is provided with the understanding that no fiduciary relationship exists because of this report. Opinions expressed in this report are the opinions of James Investment and are subject to change without notice. James Investment assumes no liability for the interpretation or use of this report. Investment conclusions and strategies suggested in this report may not be suitable for all investors and consultation with a qualified investment advisor is recommended prior to executing any investment strategy. Past performance is not indicative of future results. All rights reserved. Copyright © 2023 James Investment.